Top 3 Factoids for Your Next BevAlc Strategy Meeting

The traditional adult beverage category is fracturing. During a recent BevAlc Commerce Initiative (BACi) virtual meeting, P2PI shared how the industry is shifting from a mono-liquid culture (where "going out" was synonymous with alcohol) to a multi-modality lifestyle.

Today’s consumers aren't necessarily leaving the category; they are diversifying their drink choices based on the specific "mode" or functional ROI they desire. To help navigate this "third lane" of consumption, here are three critical factoids from our discussion to bring to your next strategy session.

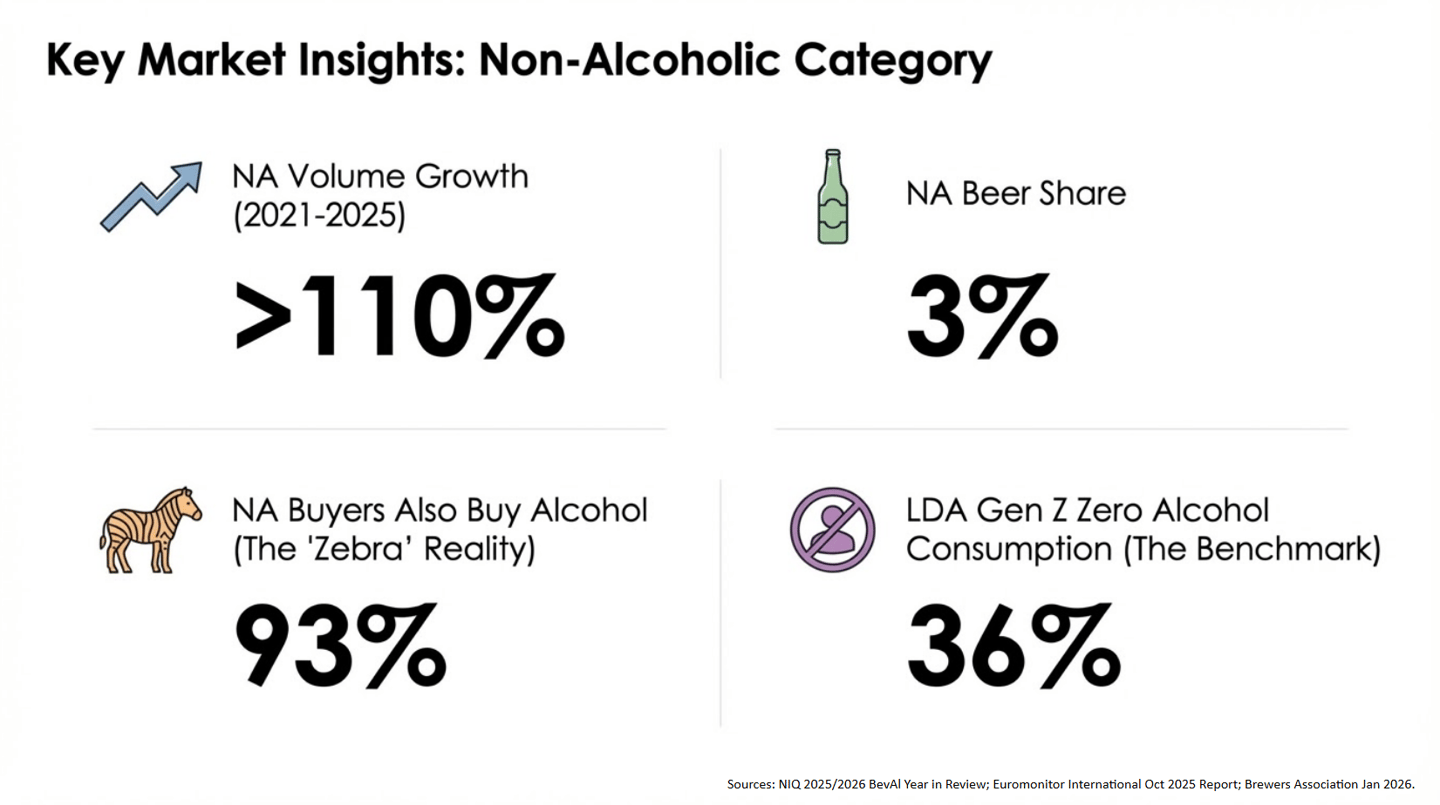

1. 93% of Non-Alc Buyers Still Buy Alcohol

The biggest misconception in the industry is that non-alcoholic (NA) products are only for non-drinkers. According to NielsenIQ, 93% of NA buyers are still active alcohol consumers. We are seeing the rise of "zebra striping," a behavior where consumers pace themselves by alternating between full-strength and NA drinks in the same shopping trip or even the same social occasion.

- The Strategy: Stop viewing NA as a vices vs. virtues choice. Instead, treat it as a pacing category. Retailers such as Target and Circle K are already leaning into this by integrating these "disruptors" into standard coolers rather than hiding them in a "lifestyle" corner.

2. From ABV (Alcohol by Volume) to ROI (Return on Ingestion)

The consumer mindset is pivoting from "How much alcohol is in this?" to "What will this drink do for me in the next hour?" According to research from Datassential, there is a 46% interest level in mood-boosting adaptogenic drinks. So, we're seeing a move toward a more functional unit model.

- The Shift: "Zero proof" isn't enough anymore; the modern consumer wants "positive proof." Whether they are seeking focus, calm or social connection, they are looking for a specific functional return.

- The Risk: This is why hemp-derived THC beverages are seeing a 58.6% substitution rate (University at Buffalo). For the first time, more than half of users say these drinks are directly replacing their nightly beer or cocktail. However, the 2026 Continuing Appropriations Act introduced a 0.4mg THC limit per container. While this loophole fix is now law, full enforcement begins in November 2026, creating crucial transition year for the third lane.

3. Gen Z Enters With a "Zero-Base" Mindset

The social contract of turning 21 has fundamentally shifted. 36% of legal-age Gen Z report never having consumed alcohol (Euromonitor). While participation increases as they gain disposable income, they enter the market with no inherent loyalty to legacy brands.

- The Digital Reality: Beverages are now viral CPGs. In Q4 of 2025 alone, drink-related categories generated $91 million on TikTok Shop, occasionally even outperforming beauty (Circana).

- The Lesson: If your brand isn’t shoppable where the consumer is scrolling, you may be missing a key discovery window. Legacy brands such as Josh Cellars are fighting back by adopting "disruptor" data tactics, using omnichannel loyalty programs to finally "own the identity" of the consumer in a model historically blinded by the three-tier system.

Whether it’s a Sunday reset occasion bundle or a THC 4-pack sitting where craft beer used to be, the third lane is claiming permanent shelf space. The question for 2026 isn't how to beat the disruptors, but how to imitate their agility.

Interested in learning more about P2PI’s BACi share group and joining the conversation? Explore now.