The Quiet Tech Shifts Behind On-Site Retail Media's Sponsored Surge

The most surprising thing about sponsored products in 2025? It's not the rise of new formats or flashy placements. It's that, over a decade in, the gap between leaders and laggards is still this wide.

Amazon's edge isn't just scale: It's also strategy. They cracked the code early, making sponsored products feel native, blending them seamlessly into the shopping experience, and driving relevance at scale.

Now we're finally seeing others — like Walmart and The Home Depot — close in on coverage. But the rest? Still playing catch-up.

Pentaleap's H1 2025 Sponsored Products Benchmarks Report reveals just how stark the divide is. A few players are optimizing infrastructure and placement logic to unlock serious advertiser value.

But most are barely past the experimentation phase. Sponsored products are retail media's flagship format —and still, the most underutilized by the majority of retail media networks.

At Pentaleap, we've been digging into the data since 2023 — and talked to our team who is building this tech —to understand what's really going on.

What's Behind the Rise in Sponsored Product Coverage?

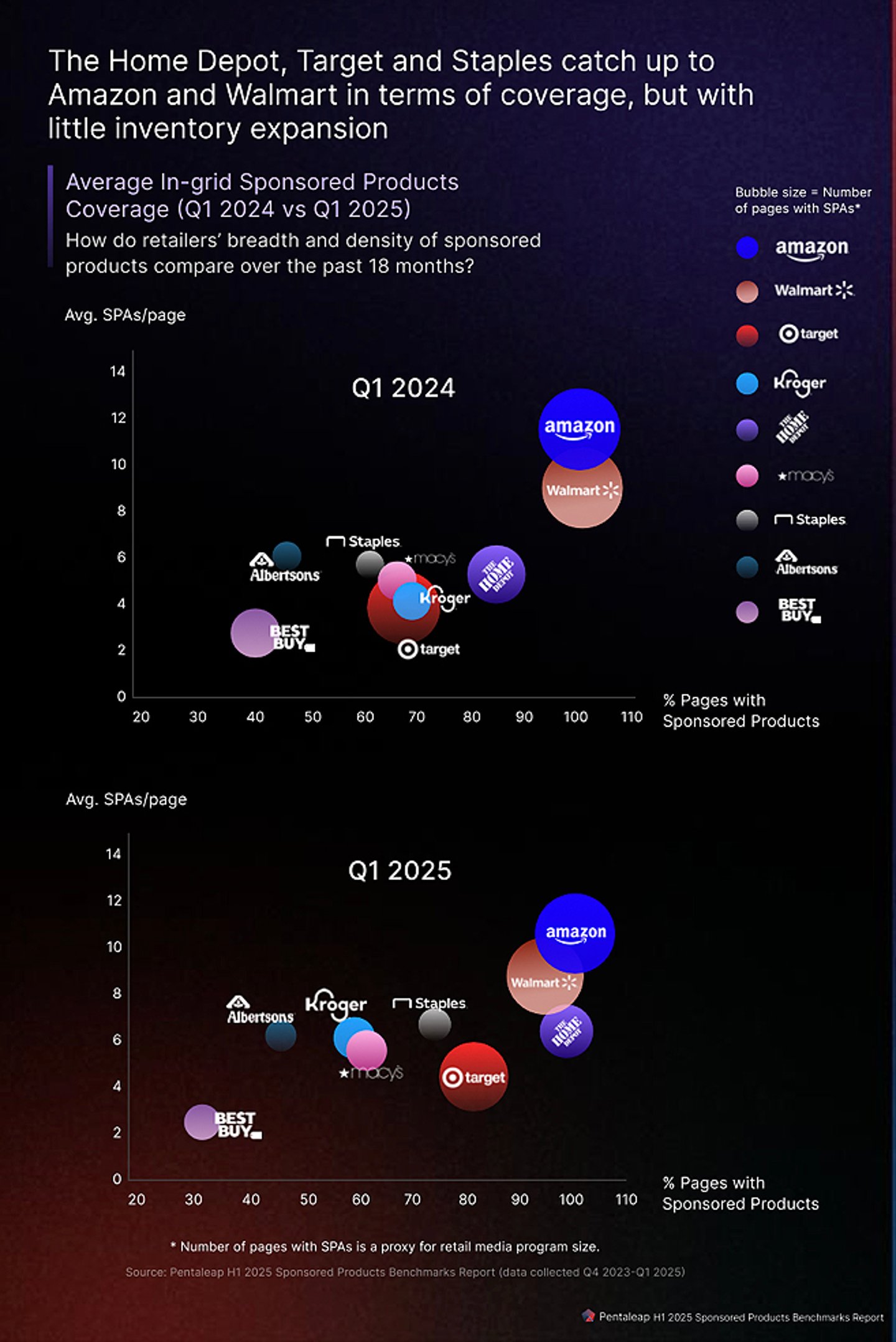

Over the past year, we've observed meaningful shifts in coverage — the proportion of product listings or pages showing sponsored ads — across several retailers, with notable increases from The Home Depot, Target and Staples. However, there has not been a corresponding increase in the number of in-grid ad slots per page.

This trend suggests a strategic focus on expanding the breadth of where ads appear rather than how many appear per page. And it raises the question: Are retail media networks optimizing performance before expanding volume?

I asked Mark Burton, chief product officer at Pentaleap, about this. He said:

"The fact that some RMNs are increasing their coverage suggests a shift towards more relevancy-based tech, which places ads across a wider array of searches. While increased demand can certainly also drive this, we'd expect to see ads per page also increase if demand was the sole factor at play — whereas this measure is mostly stable."

While we cannot determine with the publicly available data whether shifts are caused by demand growth or driven by technology upgrades — the persistent cap on in-grid ad slots implies there's still untapped potential. It also hints at a two-phase strategy:

- Phase 1: Expand coverage to prove relevancy and user experience stability.

- Phase 2: Increase slot count and scale up monetization.

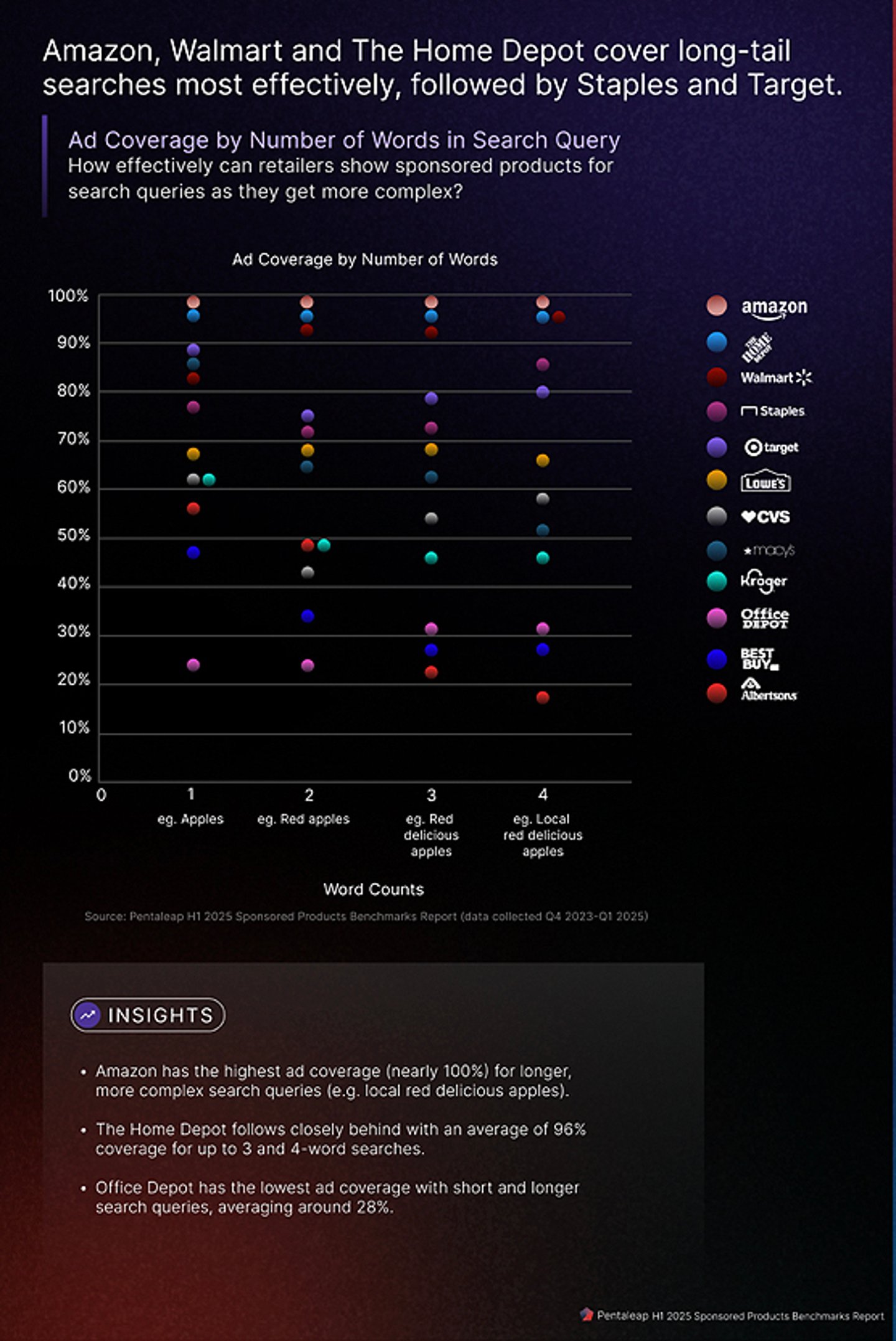

Why do Some Retailers Disappear on Complex Search Terms?

When a shopper searches for a simple term — like "protein powder" — most retailers can serve relevant sponsored product ads. But when that same shopper types something more specific — such as "plant-based chocolate protein powder for women" — many retailers fall short. Why? It comes down to the tech under the hood.

Pentaleap CEO Andreas Reiffen said: "Older retail media platforms still operate like early Google Search Ads: keyword-based. Advertisers have to manually enter every possible keyword they want their product to appear for. That might work for a few core terms — but it completely breaks down when faced with real-world shopper behavior, where queries often contain 3, 4 or even 5 terms."

Retail media networks relying on keyword-based targeting for sponsored products might see a dramatic drop in coverage, as we see in the chart below.

"Meanwhile, modern platforms work more like Google Shopping," Reiffen said. "Advertisers don’t have to guess keywords — they just say, 'promote this product.' The system uses intelligent matching, often informed by the retailer’s own site search engine, to map that SKU to thousands of relevant queries in real time. This enables far more consistent ad coverage — especially for long-tail, high-intent searches."

The key difference?

Legacy keyword targeting requires manual effort to anticipate shopper language.

Modern product-based tech automatically learns and adapts to it.

And that's why some retailers dominate, even on niche, complex searches — while others vanish entirely.

Are New Formats Just Fluff — or a Play For Bigger Budgets?

Since our H2 2024 Sponsored Products Benchmarks Report, we see a few retailers experimenting with new format: CVS, Best Buy and The Home Depot have added brand carousels.

By no means is this a reinvention of the ad format wheel. But it does signal that retailers are quietly expanding beyond standard sponsored products to attract a different kind of spend.

Onsite media has long lived off trade budgets — tied to promos, performance and shopper dollars. But brand budgets? Those are bigger, broader and historically spoken for by TV, social or upper-funnel digital. By offering more premium formats — like brand-owned placements — retailers are saying: We can do brand-building too.

From our standpoint, this isn't just a cosmetic change. It's a strategic one. It's a shot at grabbing a slice of that brand budget while keeping media spend onsite.

And let's be honest: Advertisers expect more than "pay to play" endcaps and circulars. They want tools that feel like the platforms they already use — Amazon, Meta and more. This isn't just about visibility anymore. It's about positioning retail media as a true contender for brand dollars.

About the Author

Sarah MacKinnon leads product marketing at Pentaleap from a sunny office in the south of Spain. An ad tech nerd with a decade of B2B SaaS research and content development under her belt, she spends offline hours hiking, swimming in the Mediterranean and sewing her own wardrobe.