Report Examines the Evolving Landscape of Health and Beauty

As health and beauty shoppers’ needs and purchasing patterns evolve, CPG brands are taking an attribute-driven approach to deliver what’s important to their target consumers (e.g., clean label, cruelty free and vegan ingredients).

A recent report from market research firm NielsenIQ examines how brands can determine which characteristics will drive category sales on which channels, and how to expand beyond traditional demographics and reach new consumers.

Considering the growth of the personal care category, including the widening array of products available across health and beauty segments, addressing consumers’ evolving needs and preferences can present myriad challenges for brands trying to improve their market share.

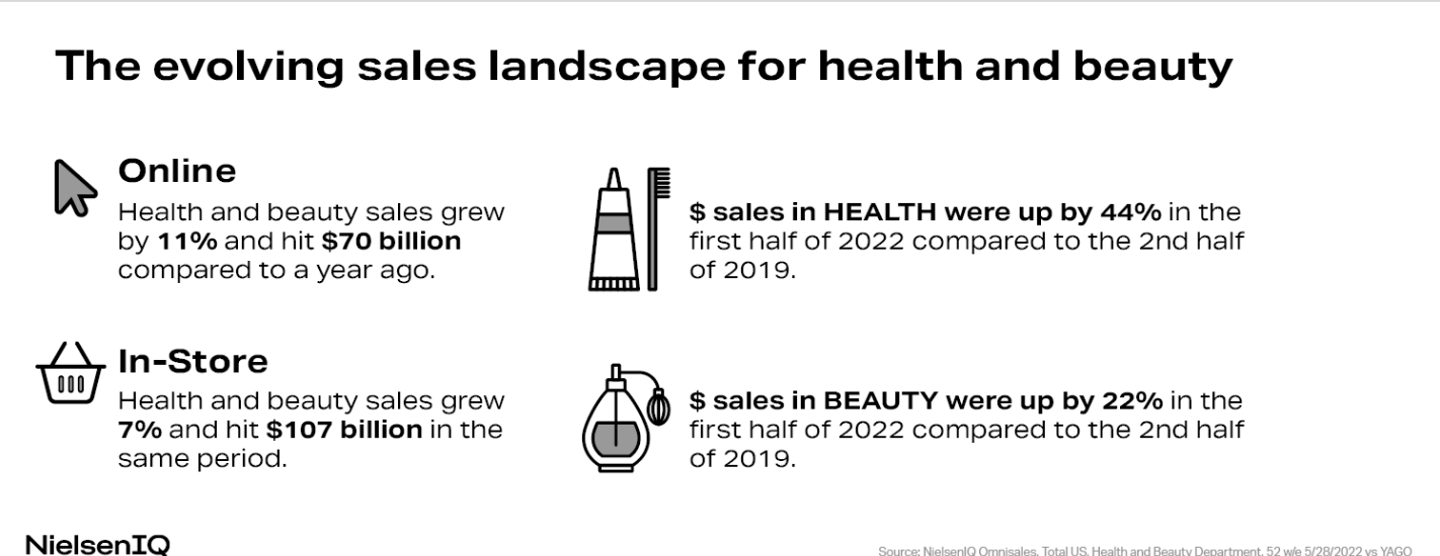

For CPG manufacturers with products in the personal care category, online is more important for their sales than ever, according to NielsenIQ’s reporting. Like many categories, growth in the online channel is outpacing in-store. NielsenIQ Omnisales data found that in the 52 weeks ending May 28, online health and beauty sales hit $70 billion, an 11% increase over one year ago, and in-store sales hit $107 billion, a 7% increase.

The fastest overall growth in the same period came from categories like medical accessories (+61%), upper respiratory (+38%), ear care (+23%), fragrances (+16%) and sun care (+15%).

Some other key points and data outlined in the report include:

- Consumers have adopted a more flexible shopping routine since the pandemic, often combining in-person and online trips. However, according to NielsenIQ Omnichannel Shopper data from 2022, 68% of consumers insist on purchasing certain items in-store, like personal care, produce, bakery, meat and seafood, and clothing.

- During the Amazon Prime Day period in July 2022, 37% of consumers surveyed by NielsenIQ said they purchased beauty and personal care products. Major online sales events like Prime Day have inspired other retailers to run sales both online and in physical stores, further blurring the lines between e-commerce and brick-and-mortar.

Additionally, consumers across demographics are engaging more with wellness-focused content and products, which has become a cornerstone of the health and beauty industry today. Their needs have evolved beyond the basics of physical well-being, and have increasingly drove consumers to indulge more in self-care, preventative care, innovative care and “selfless care,” based on the products they buy and brands they support.

When it comes to generational shifts, NielsenIQ noted that:

- Shipped/delivery orders and curbside pickup also increased as consumers first pulled back on in-person shopping and embraced the other shopping methods. Notably, consumers of all ages and backgrounds have developed new behaviors focused on convenience, saving time and maximizing their choices.

- Within the health and beauty category, Millennials and consumers with a higher income are most likely to shop online. Only 10.1% of OTC health product sales in-store come from consumers under 35, while 42.4% come from consumers over age 55.

- Younger shoppers have also showed openness to try new products. Many consumers under 35 have shown interest in trending items like topical analgesics and natural upper respiratory products. They’re also more willing to shop online through click-and-collect or use services such as Shipt and Gopuff.

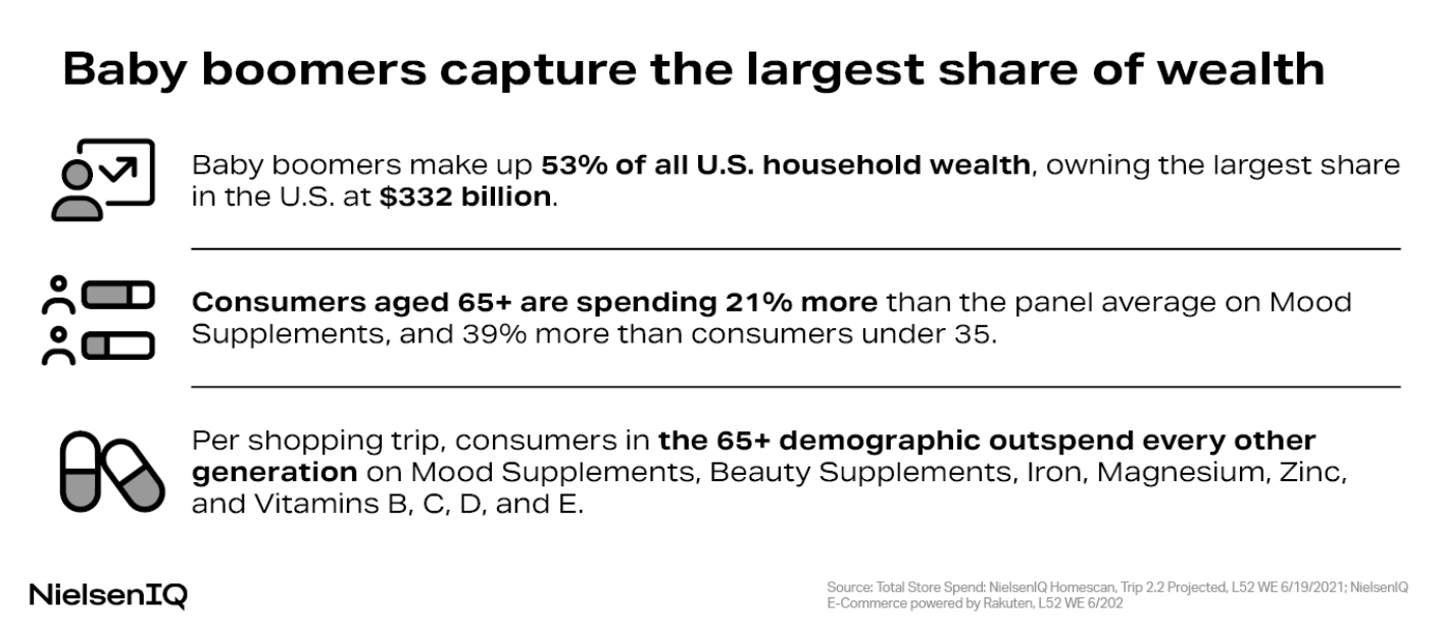

- Baby Boomers also present brands with new opportunities. They had the largest share of wealth in the U.S., $332 billion, for the 52 weeks ending June 19, 2021. Boomers make up 53% of all U.S. household wealth, according to NielsenIQ Homescan data.

- Boomers tend to favor the traditional drug and club stores when shopping in-store for OTC items, but they are the fastest growing group of e-commerce shoppers.

Additionally, in the 52 weeks ending June 18, women made up 52% of the total buyers in omni health and beauty sales, 52% in-store sales, and 57% in online sales. NielsenIQ’s data also shows that women spend 33% more in the category than men overall and nearly 70% more online.

Consumers also want to see authentic marketing from brands in period care and incontinence. NielsenIQ’s data also highlighted indie brand The Honey Pot Company for advertising its plant-derived products with realistic depictions of periods and sexual health education. The brand’s sales have grown by $100 million over the last two years, positioning it as a force in the category.

Period care and adult incontinence products that are better for the environment with safer ingredients are significant health and beauty care trends in the sexual wellness category. Emerging trending attributes for these items include “100% recycled paperboard,” “shea butter” and “biobased product certified.” Period care products that are “premium” have grown by 25%, “recycled packaging” has increased by 13%, and “free from phthalates” has grown by 6% year-over-year.

Brands have a slew of options for placing products with the right attributes or claims directly in the path of values-oriented customers, including circulars, in-store promotions, seasonal events, loyalty programs, personalized offers, digital coupons and online ads.

However, since the marketing ecosystem has become increasingly personalized and complex, it’s crucial brands in the evolving health and beauty landscape have a big opportunity to reach beyond traditional customer demographics and activate consumers on and offline. View more of NielsenIQ’s reporting here.