Path to Purchase Trends 2025, Part 2: Social Media, AI & More

Social commerce, retail media, artificial intelligence and economic uncertainty have come to the forefront of part 2 of the Path to Purchase Institute’s 2025 Trends report.

Survey results show that brands’ investments in social media and retail media continue to rise, while their commitment to using AI has risen dramatically.

Furthermore, results show that many of the biggest business-related concerns for CPG marketers have to do with the current political and economic environment as it relates to tariffs.

While part 1 of the annual survey was conducted in late 2024 and devoted to retail media (and rating the retailer media networks), part 2 was conducted in April and May 2025 and covered a wider range of topics.

Part 2 was designed to receive the perspectives of the consumer product marketers — those directly employed by the brand companies (62% of respondents) as well as, for the first time in 2025, their agency representatives (38%).

More than 30% of respondents identified shopper marketing as their primary job function. Other job functions mentioned the most include insights/research/analytics (16%) and brand marketing/advertising/consumer promotions (16%).

Meanwhile, 40% identified as working at the manager level, followed by 29% at director and 13% at senior management.

Retail Media & Social Media

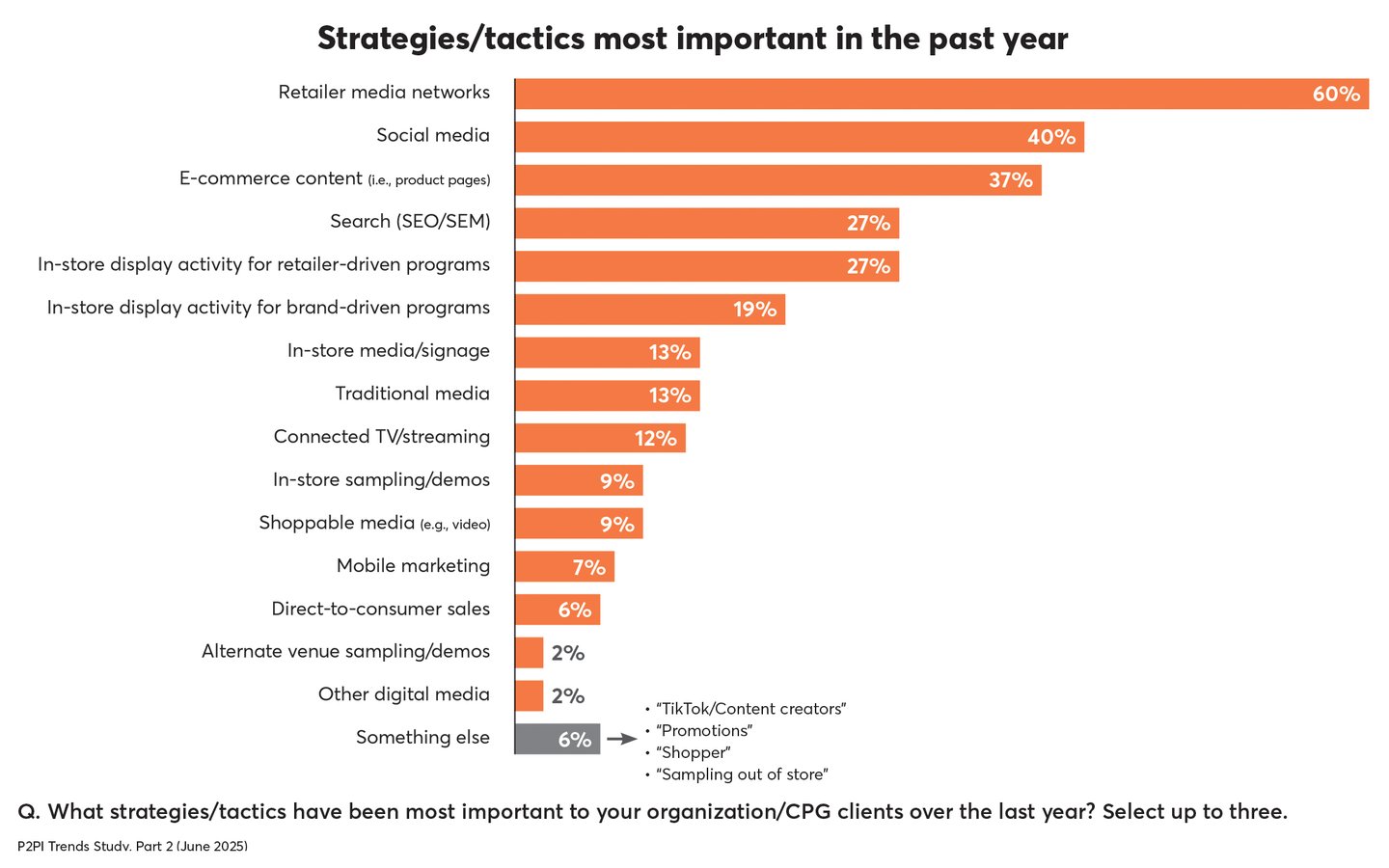

Early on in the survey we asked what strategies or tactics have been most important to survey takers’ organizations (or to their clients) over the last year. Respondents could choose up to three responses from the list we provided, or write in their own.

Retailer media networks rose to the top this year, with 60% of respondents selecting that strategy/tactic as having been most important (compared to 40% in 2024’s survey).

Social media (40%) and e-commerce content (37%) were next in line, with e-commerce having dropped from 48% in our 2024 survey.

The percentage of respondents who chose social media as a strategy/tactic that was most important in the last year was consistent from 2024’s survey.

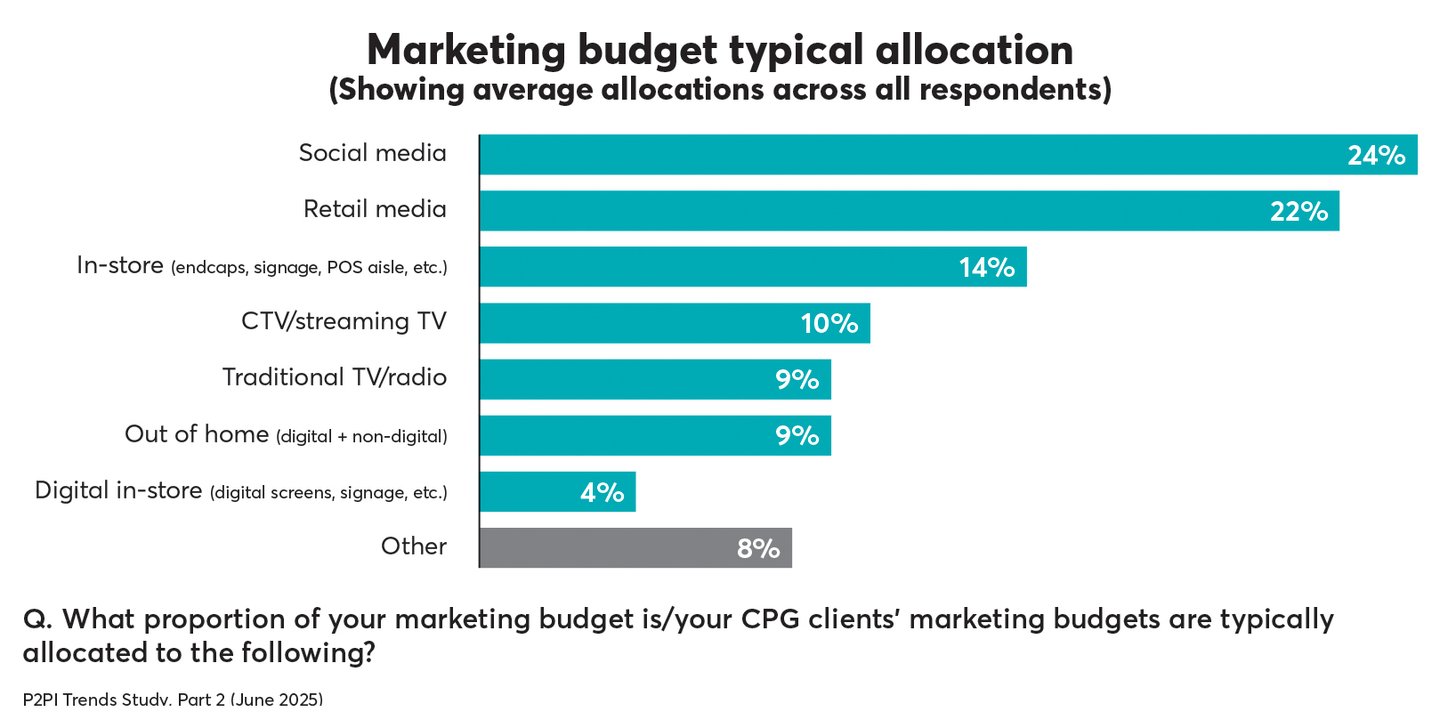

When we asked what portion of their marketing budget is typically allocated to various tactics, social media (an average of 24% across all respondents) and retail media (22%) outpaced others.

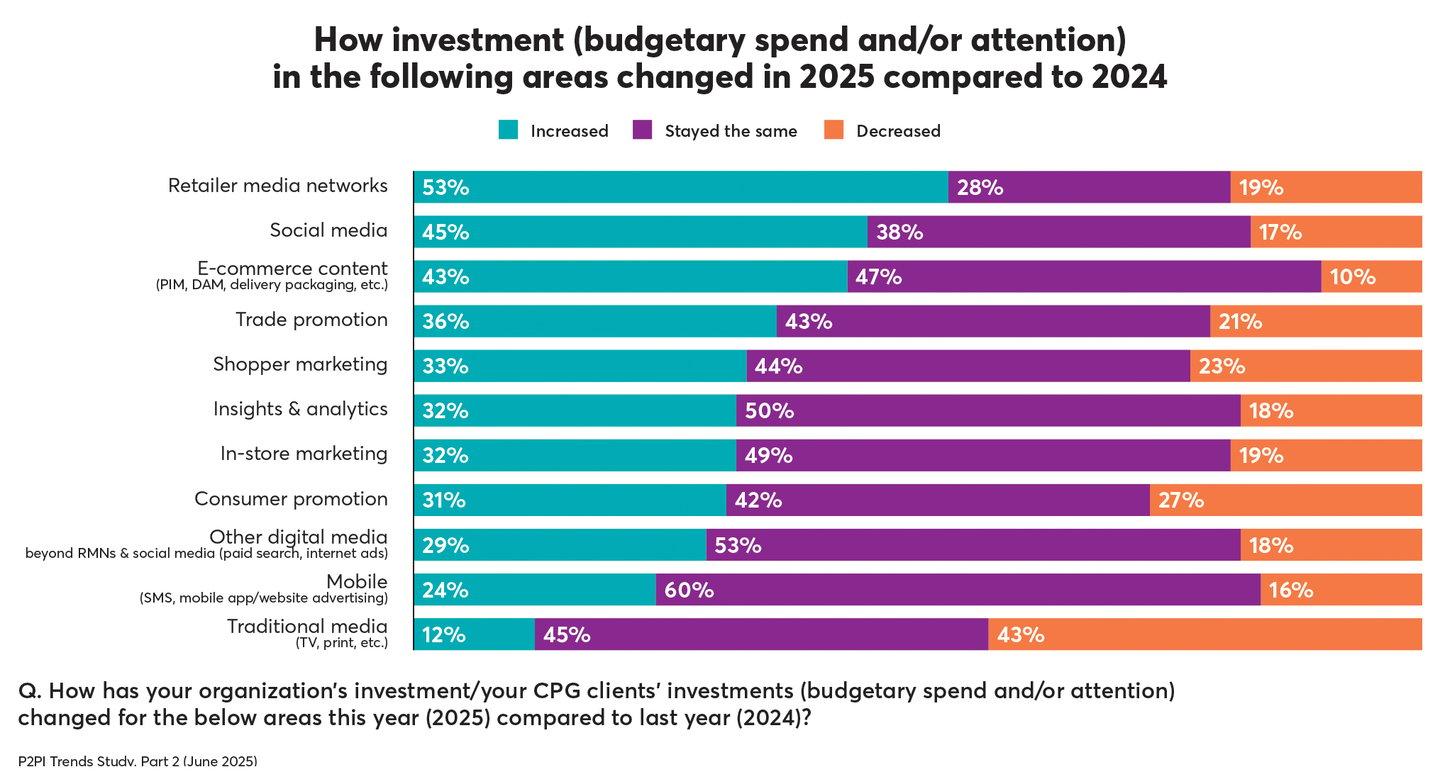

For the second straight year, retailer media networks (53%) and social media (45%) topped the list of tactics for which respondents said they increased their investments — although the number who said they increased their investments for each was lower in 2025 than in 2024.

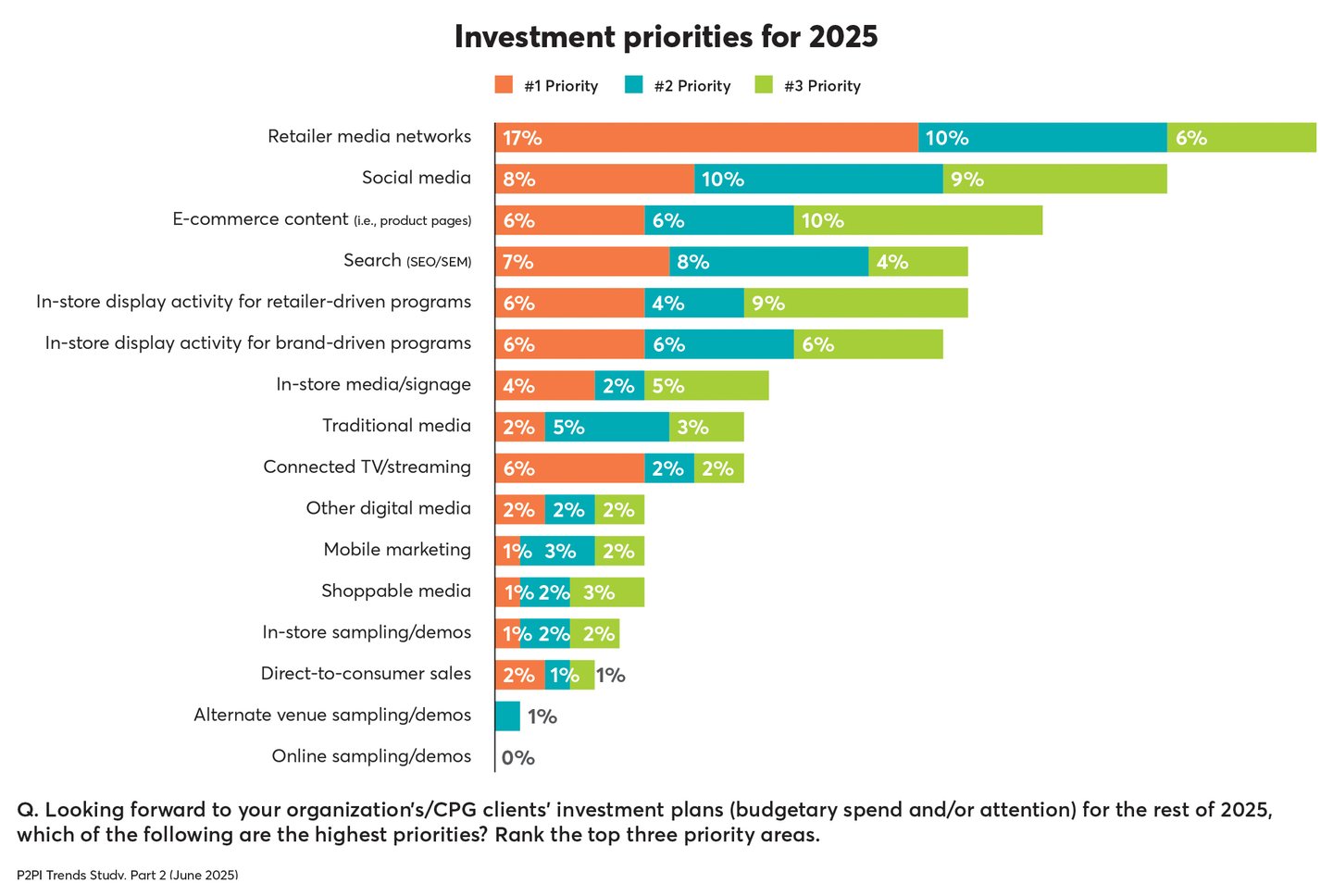

When asked which tactics are their highest priorities for the remainder of 2025, respondents selected retailer media networks and social media as top-3 priorities more than any other tactic. Retailer media networks were selected by 33% (17% said it was their No. 1 priority, compared to 6% in 2024), and social media was selected by 27%.

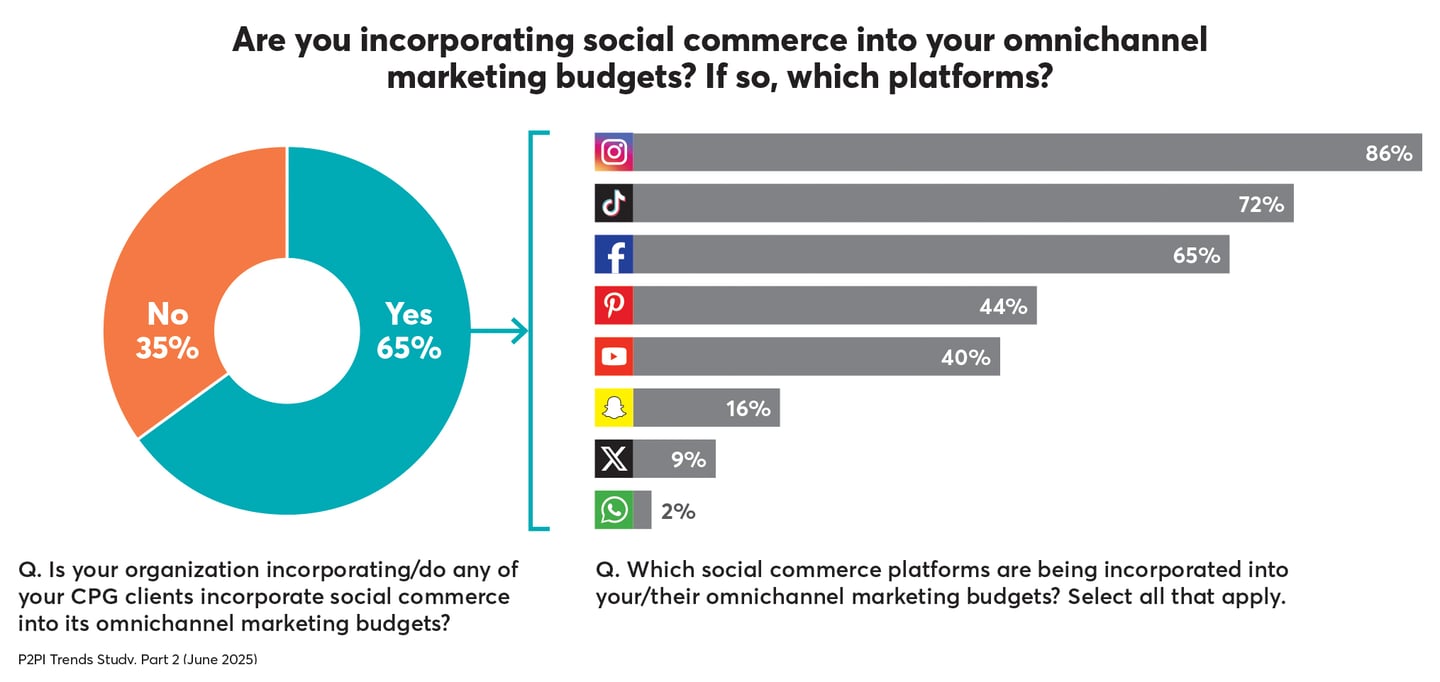

Diving deeper into social media/commerce, 65% of respondents said they incorporate social commerce into their omnichannel marketing budgets, consistent with our 2024 survey.

Among those survey participants incorporating social commerce into their omnichannel marketing budgets:

- 86% said they incorporate Instagram into their budgets, followed by TikTok (72%) and Facebook (65%).

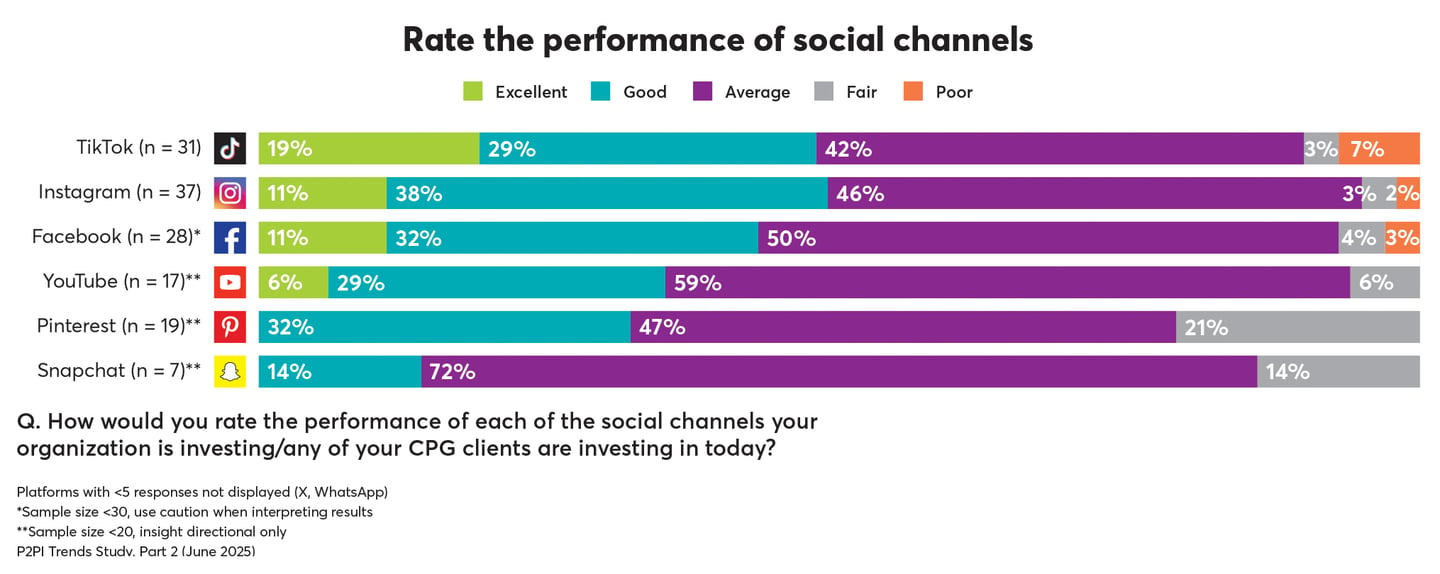

- 32% or more rated each of the specific social channels as performing good or excellent (except for Snapchat). TikTok led the way with an excellent rating of 19%.

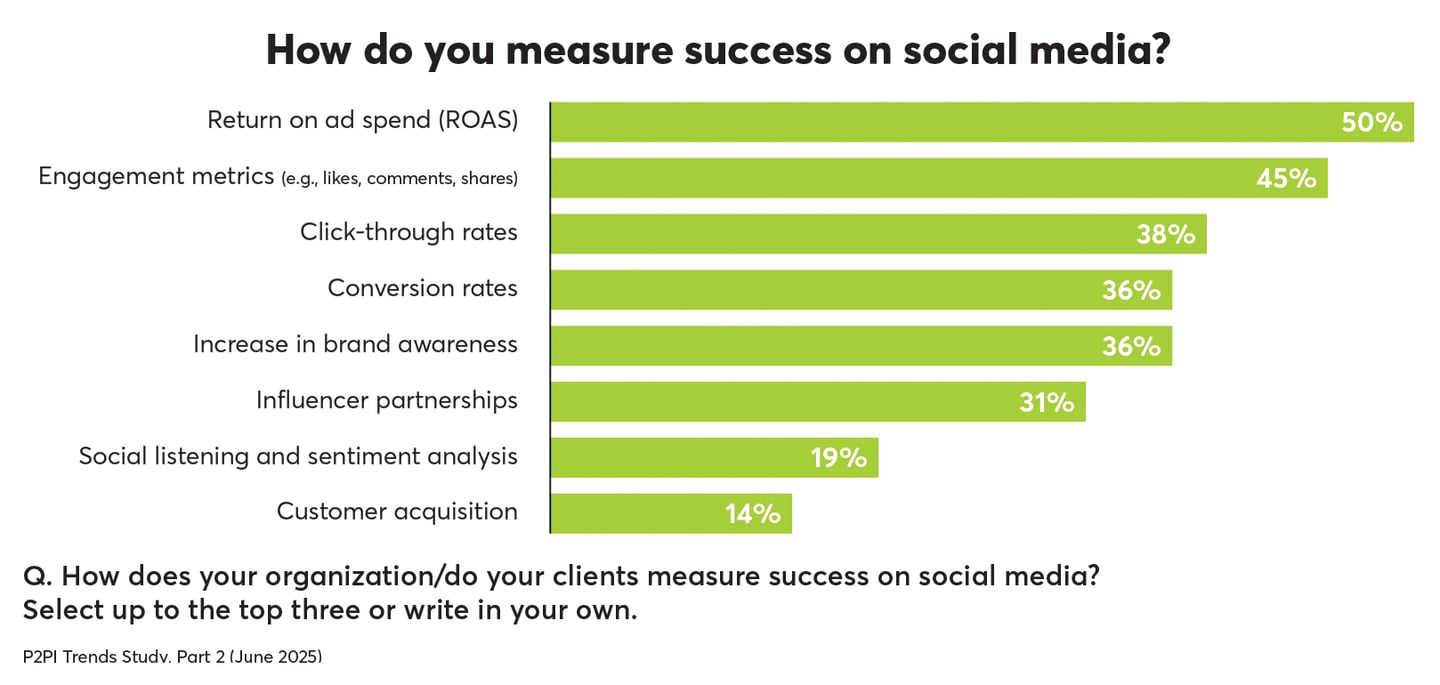

Interestingly, when asked how they measure success on social media (and to pick three measurement tactics from a list of eight), respondents incorporating social commerce into their budgets showed no consistency: Return on ad spend received 50% closely followed by engagement metrics (e.g., likes, shares) with 45%. Otherwise, click-through rates, conversion rates, increase in brand awareness and influencer partnerships received at least 31%.

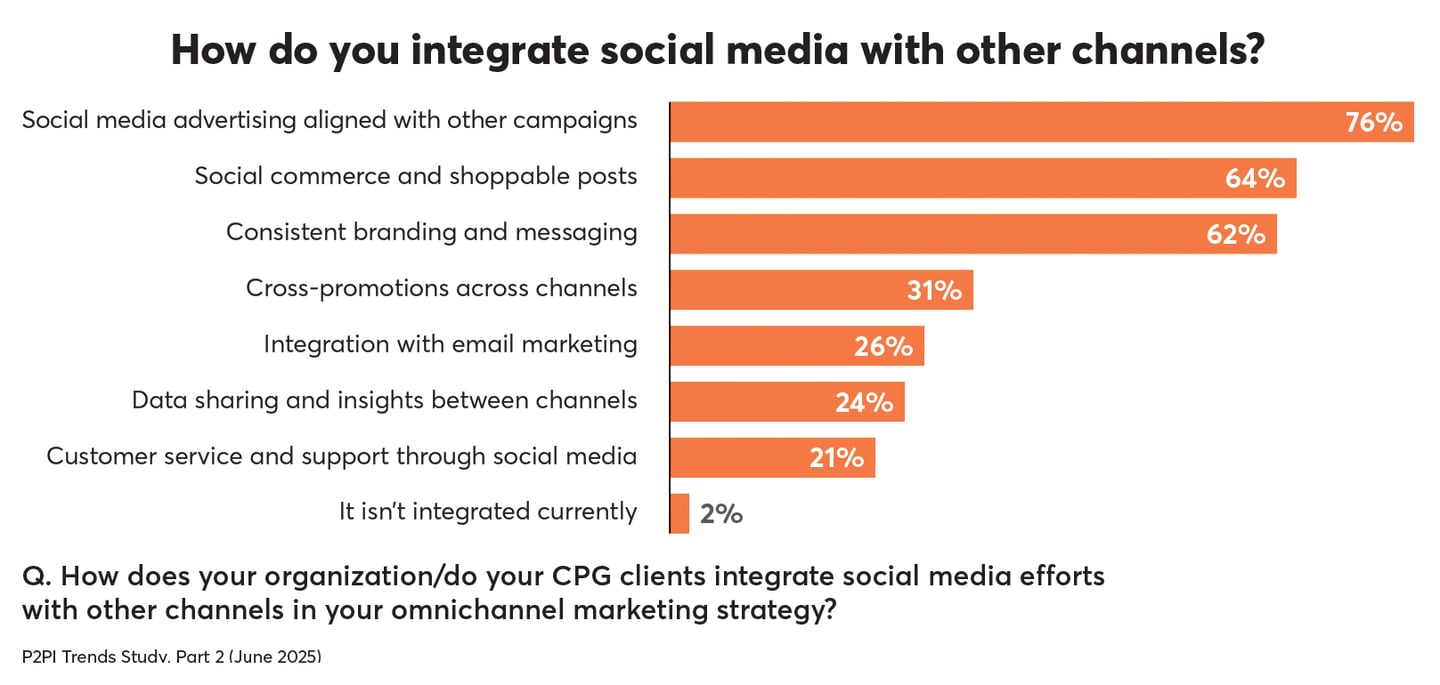

Furthermore, when asked how they integrate social media efforts with other channels in their omnichannel marketing:

- 76% said their social media advertising aligns with other campaigns.

- 64% said they use social commerce and shoppable posts.

- 62% said they use consistent branding and messaging.

Artificial Intelligence

Again this year we devoted one section of the survey to artificial intelligence (AI).

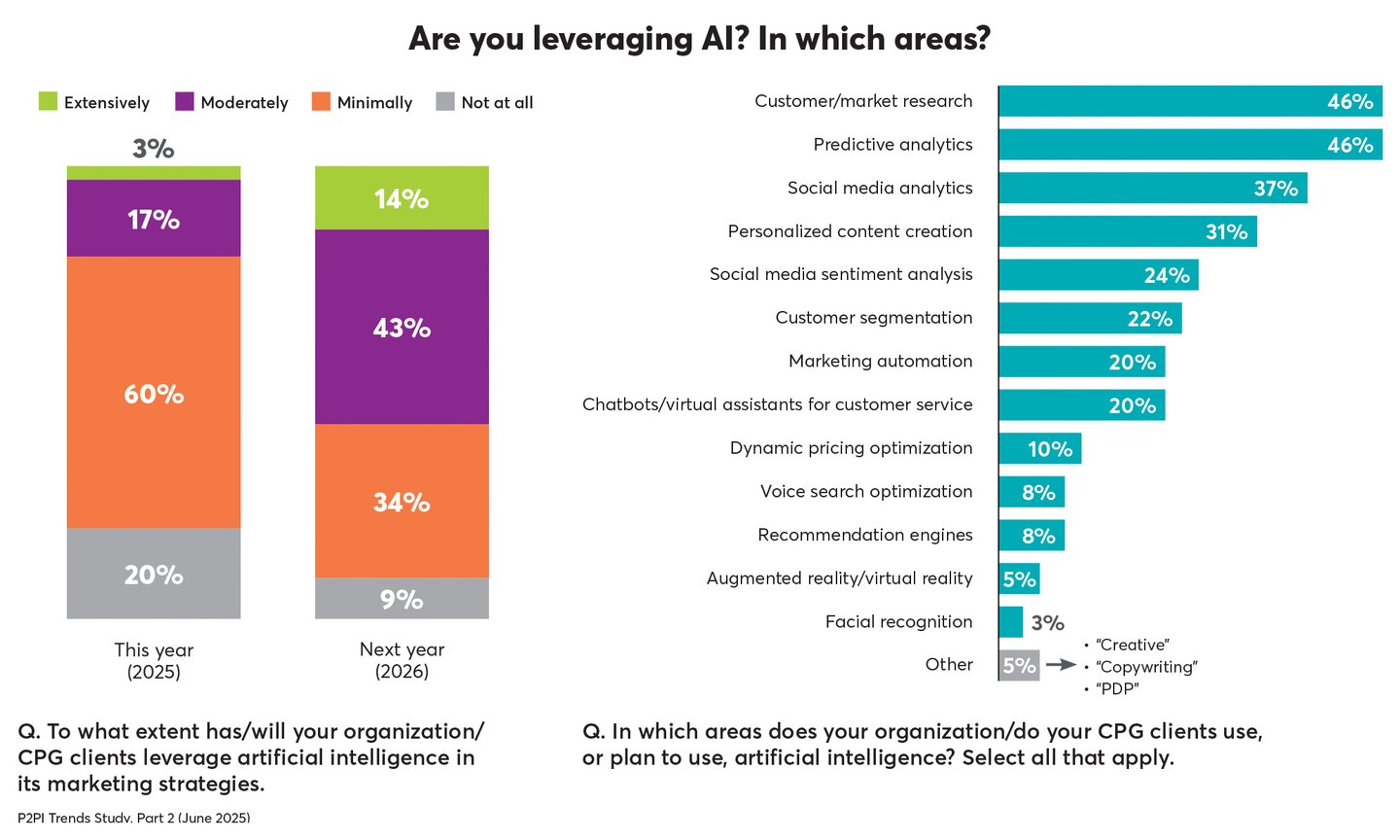

We first asked to what extent they use (and plan to use) AI in their marketing strategies. Eighty percent said they at least minimally use AI now, and 91% said they will in 2026. In our 2024 survey, 41% said they weren’t using AI at all.

We asked respondents in which areas they use, or plan to use, AI. Selecting from a list of 13 possibilities, they most often said customer/market research (by 46%), predictive analytics (46%), social media analytics (37%) and personalized content creation (31%).

When asked to expound on their use of AI, many said it was well-suited to support content creation. Others mentioned targeting, analytics and pricing support.

“We use it as a starting off point for messaging, then adapt it to be more clearly in strategy and right for a specific brand,” wrote one respondent.

“This is an early discussion for us, thus, we are trying to figure out how to incorporate it for our business,” wrote another.

Another wrote: “It's more for use on the back end and optimizing behind the scenes, rather than being consumer-facing.”

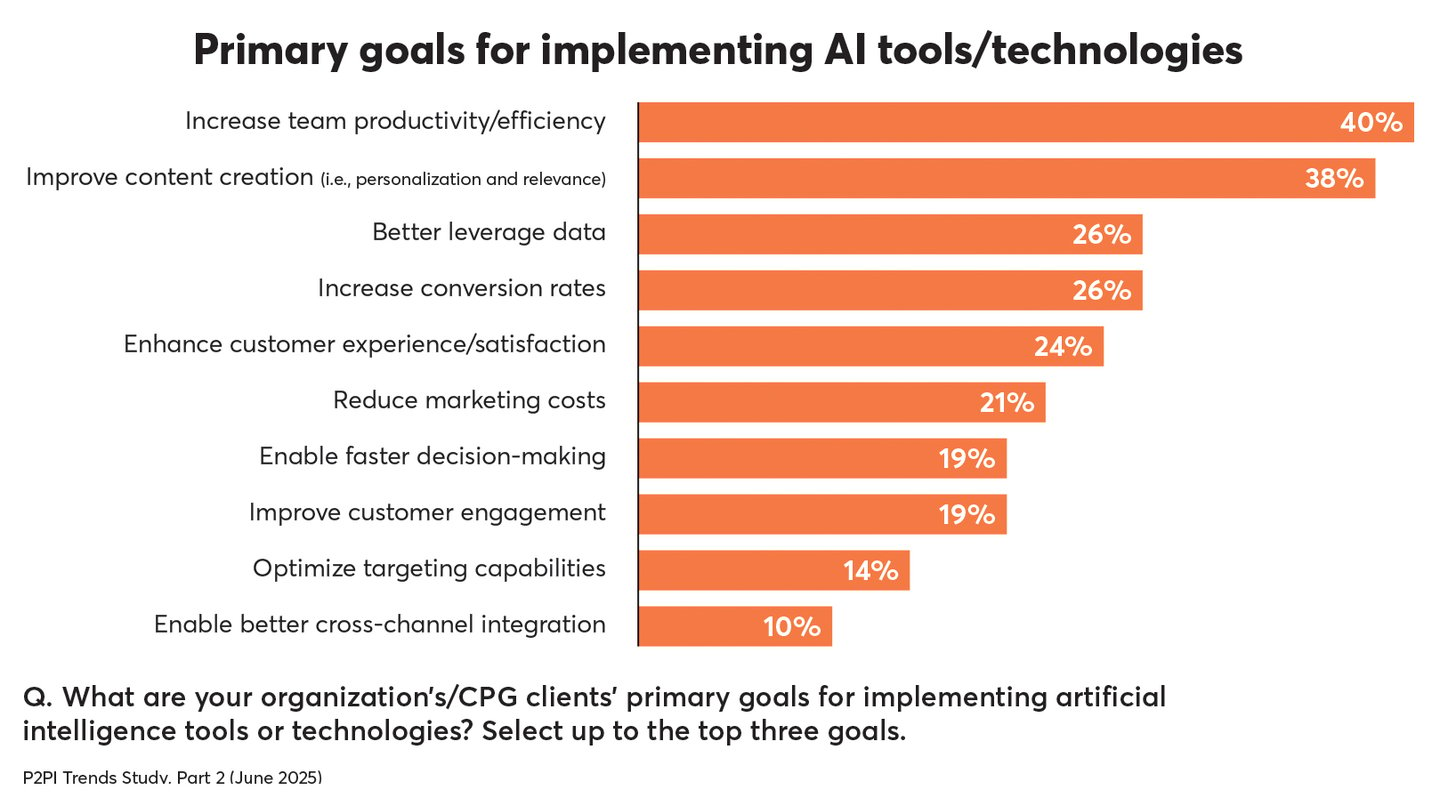

Asked to select up to three of their primary goals for implementing AI tools and technologies from a list, respondents most often selected to increase team productivity/efficiency (40%), improve content creation (38%) and better leverage data (26%).

2025 Business Concerns

Question 1 in our survey was, “What’s your (or your clients’) biggest business-related concern this year?” For many, the uncertainty due to the current political/economic environment as it relates to tariffs was top of mind.

Here is a sampling of responses:

“Tariffs, consumer sentiment/confidence and pulling back of purchasing in certain categories. Overall lingering recession.”

“Volatility in the economic environment due to tariffs and price. … Ability to make investment decisions in an uncertain environment.”

“Tariffs and how to fund without eroding consumer demand or operational investments in order to support revenue.”

“The uncertainty and impact of tariffs, which is causing a need to reduce marketing budget and do more with less.”

Going beyond those types of responses, some responses were fast and simple, while others a bit more in-depth:

“Conversion/sales.” ... “People consuming less.” ... “Retail media shifts. AI. Commerce trends. Measurement.”

“The path to purchase is increasingly non-linear, spanning digital, social and physical touchpoints — with tight budgets in mind and more investment ask from retailer partners. How do we balance our investment and where do we focus efforts and budgets to reach consumers and shoppers while meeting ROIs?”

Other Insights

While our annual survey repeats many of the questions year over year, we do introduce new questions/topics.

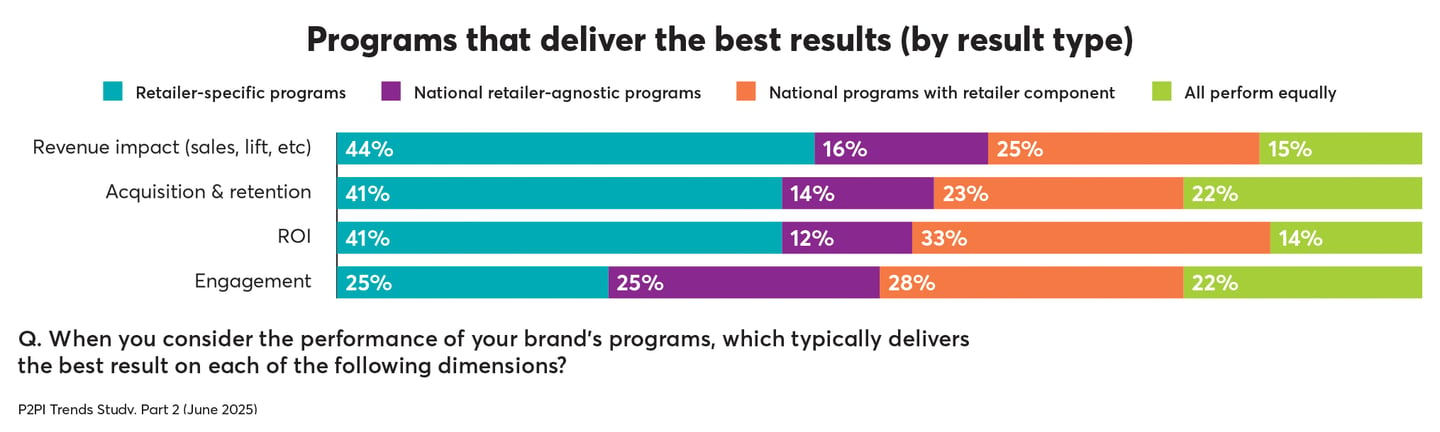

This year, with one of the new questions, we asked which type of brand programs typically deliver the best results (i.e., revenue impact, acquisition & retention, ROI and engagement).

While some respondents indicated that they all perform equally, many more showed a preference. Retailer-specific programs, followed by national programs with a retailer component, clearly outpaced retailer-agnostic national programs for revenue impact, acquisition & retention and ROI, but not for engagement.

With another new question, we asked respondents if their brands were realizing more or less value from retailers’ loyalty programs compared to a year ago. Thirty-nine percent said they were realizing more value, while 52% said it’s about the same.

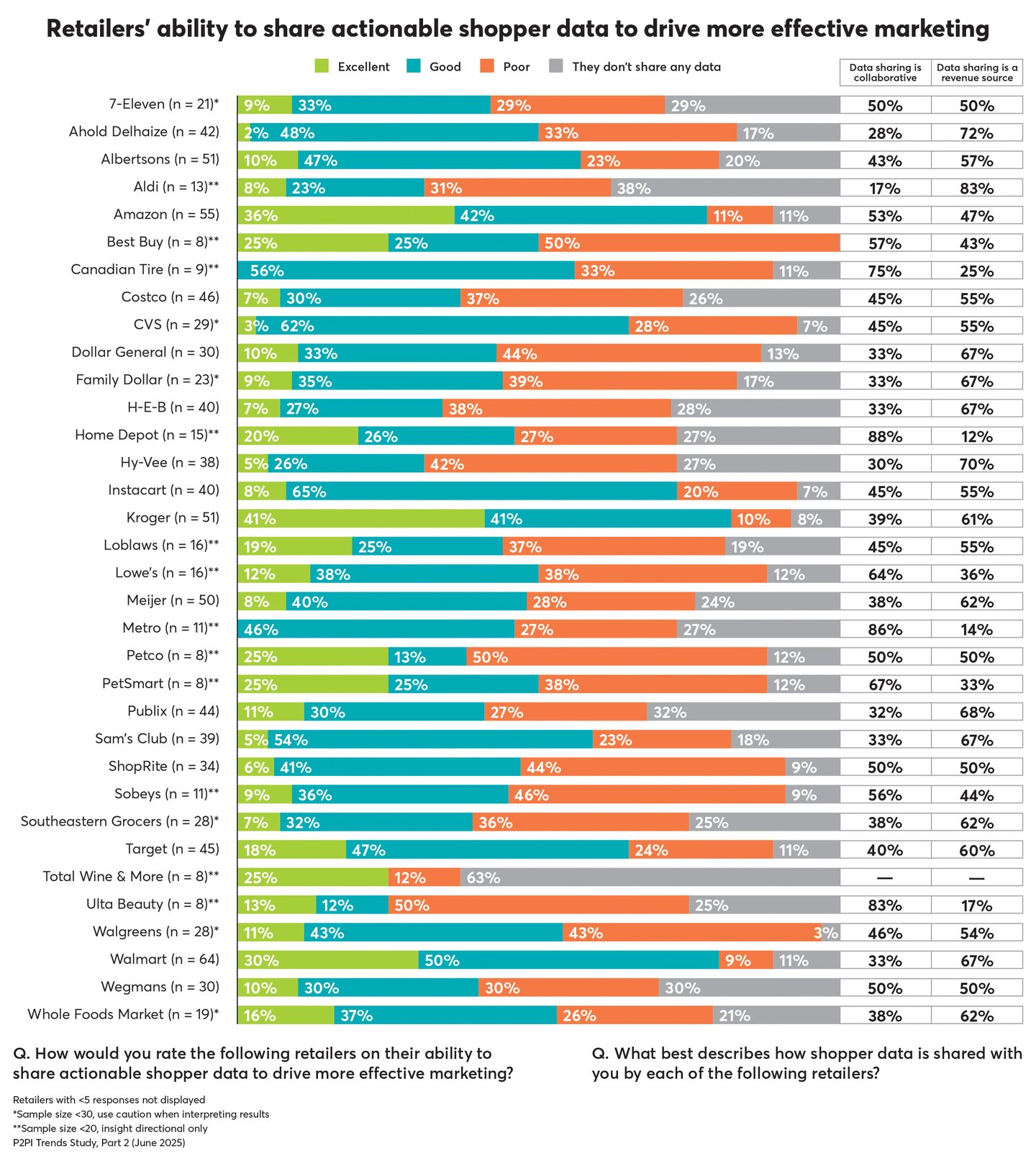

Meanwhile, one of the topics we repeat year after year: After identifying which retailers they’ve worked with in the last year, we asked respondents to rate those retailers on their ability to share actionable shopper data to drive more effective marketing. Kroger, Walmart, Amazon, Instacart and Target were each identified as excellent or good by two-thirds or more of respondents who worked with them.

The Home Depot, Metro, Ulta Beauty, Canadian Tire, PetSmart and Lowe’s were called out the most for their data sharing being collaborative, as opposed to a revenue source.

- Interested in more?

The full findings from part 2 of our 2025 Trends report are available to P2PI members in the “P2PI Research” section on our website.