Special Report: Path to Purchase Trends 2024, Part 2

There’s no denying that retail media has been and continues to be one of the hottest topics in commerce marketing. Look no further than part 2 of this year’s Trends survey to drive that point home.

For the 2024 version of the Path to Purchase Institute’s annual Trends survey, we decided to split our survey into two parts, with the first part dedicated to retail media and the retailer networks (see the January/February issue). Part 2 would be focused more on the general and traditional trends in commerce marketing, like budgeting and in-store marketing, as well as more futuristic topics such as artificial intelligence.

Well, despite that approach, after poring over the survey results, we felt inclined to bring retail media to the forefront of this report as well.

For part 2 of our survey, we interviewed 80 consumer product marketers from Dec. 19, 2023, through Jan. 22 of this year. More than 40% of respondents identified shopper marketing as their primary job function, with 33% indicating they were at the director level, and 48% at the manager level.

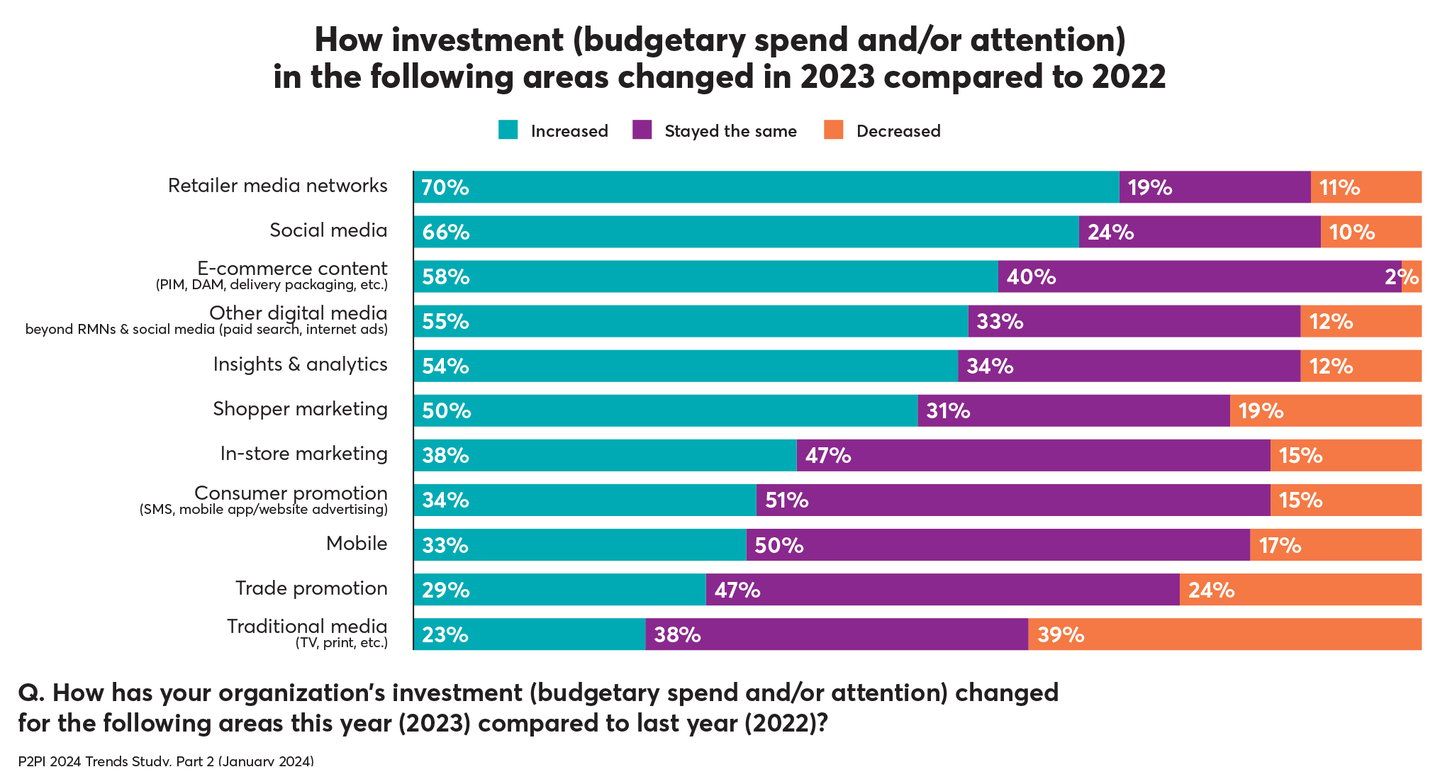

When asked how their organization’s investment in certain areas had changed in 2023 vs. 2022, 70% of respondents said their investment in retailer media networks had increased, the most for any area we identified. Social media (66%), e-commerce content (58%), digital media other than retail media (55%) and insights & analytics (54%) were the other areas most identified as having increased.

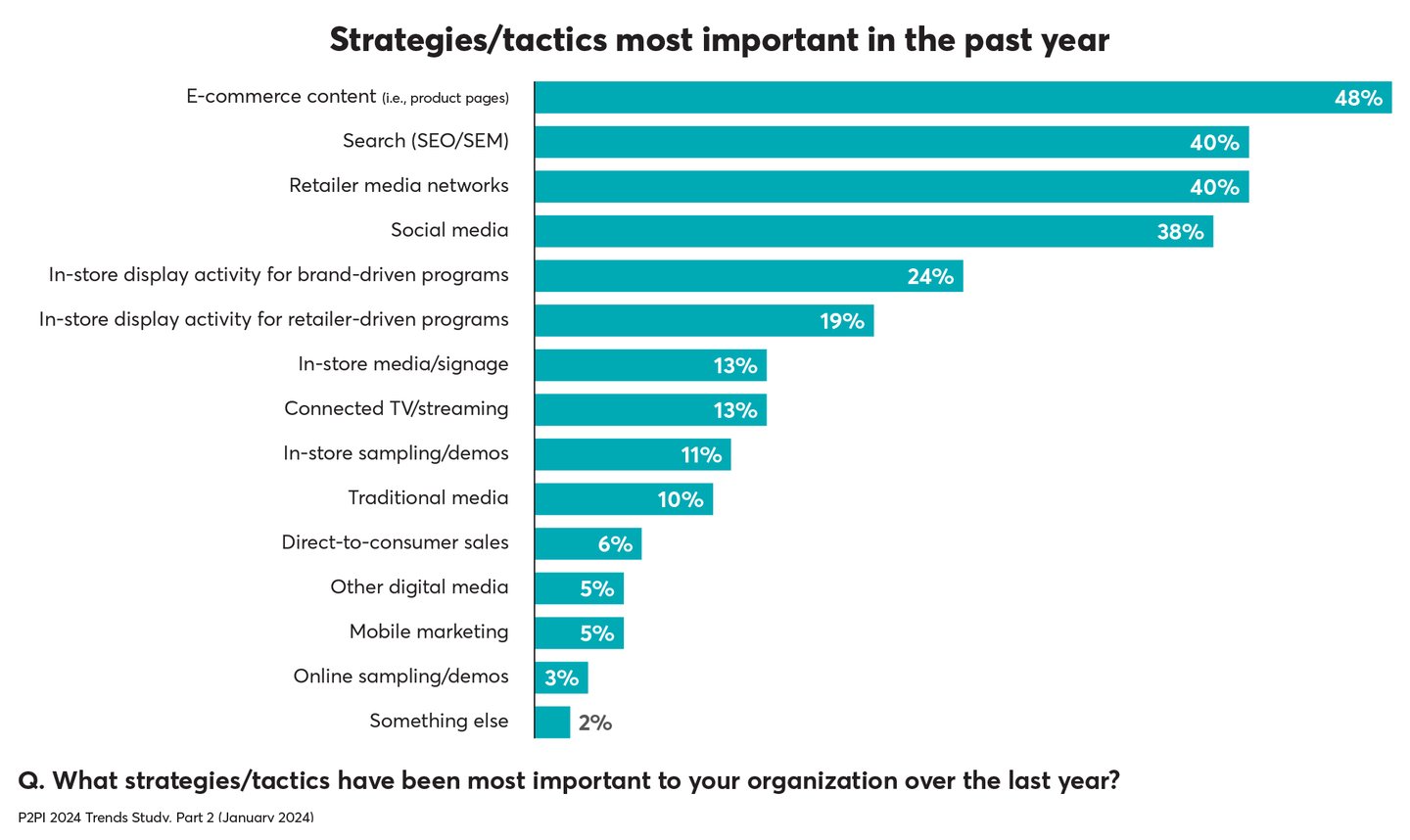

Furthermore, when asked to select up to three strategies/tactics from our list that have been most important to their organizations in the last year, 40% identified retailer media networks. Only e-commerce content (48%) was selected more, while search (SEO/SEM) and social media garnered similar percentages to RMNs.

Asked to explain why they chose their three particular tactics, respondents who selected RMNs offered:

“We’ve invested more in retail media networks, in-store signage and promotion where possible, and digital media in general to increase brand awareness and increase market share.”

“We are investing further into retail media networks as a part of our total sales support package with key retail partners.”

“Increased focus on incrementality/efficiency with ROAS. Increased focus on in-store and retail media networks. Increased focus on profitability.”

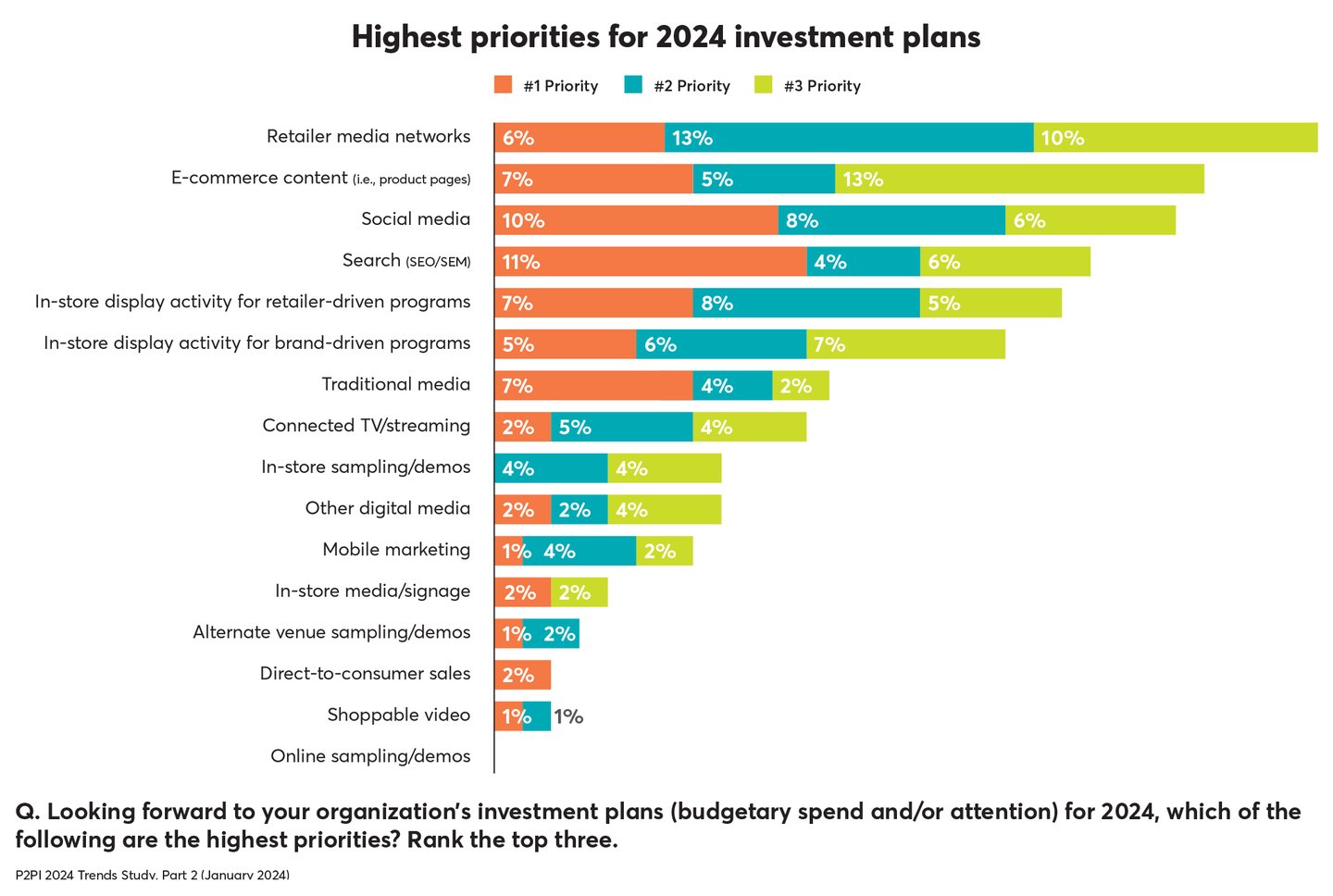

And looking ahead to 2024, 29% of respondents said retailer media networks are one of their organization’s top three priorities from a list of tactics, again the most for any area we identified. And once again, e-commerce content, social media and search were the other tactics most prioritized.

When asked what their biggest business-related concern was heading into 2024, without us suggesting any potential answers, one-tenth of respondents mentioned retail media. “The cost of participating in retailer’s media programs, making my budget stretch as much as I can to drive strong topline sales for our brands,” answered one survey taker.

The impact of inflation on consumer spending was the most common theme among the business-related concern answers, with 34% mentioning that. Among the specific responses:

“Shoppers trading down to lower-price segments within categories, eroding brand loyalty.”

“Trying to drive growth in the current economic climate against significantly better funded competitors.”

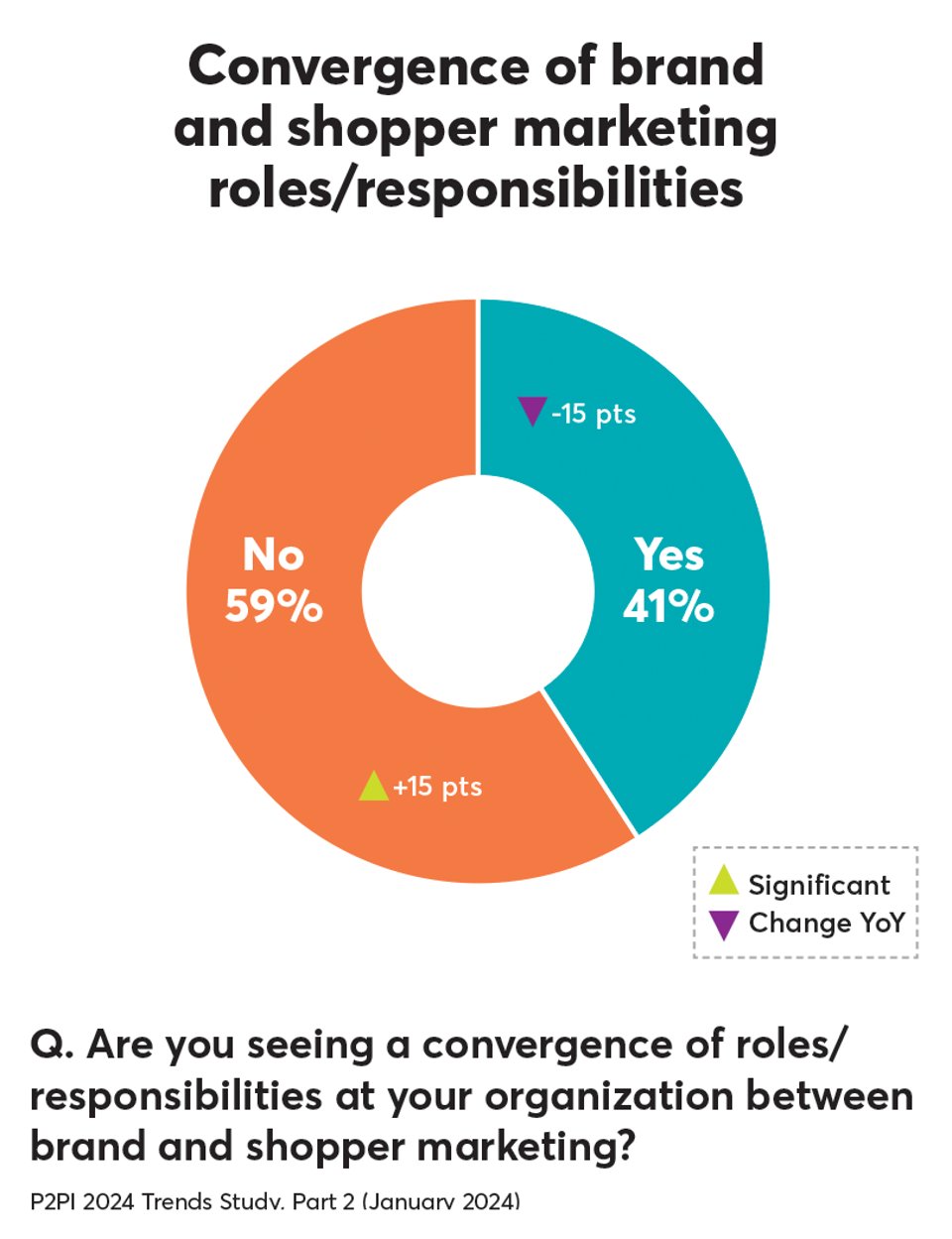

The next strategy-related question we asked was if the survey takers were seeing a convergence of the brand and shopper marketing roles/responsibilities at their organizations. Forty-one percent answered yes, a drop of 15% from when we asked the same question in last year’s survey.

“Retailer media networks are providing solutions that stretch up the funnel, so we’re working closely with our brand teams to align on overall strategies and deploy the right amount of funding to different parts of the funnel,” one person (a shopper marketer) responded to how those roles are converging.

Social Commerce

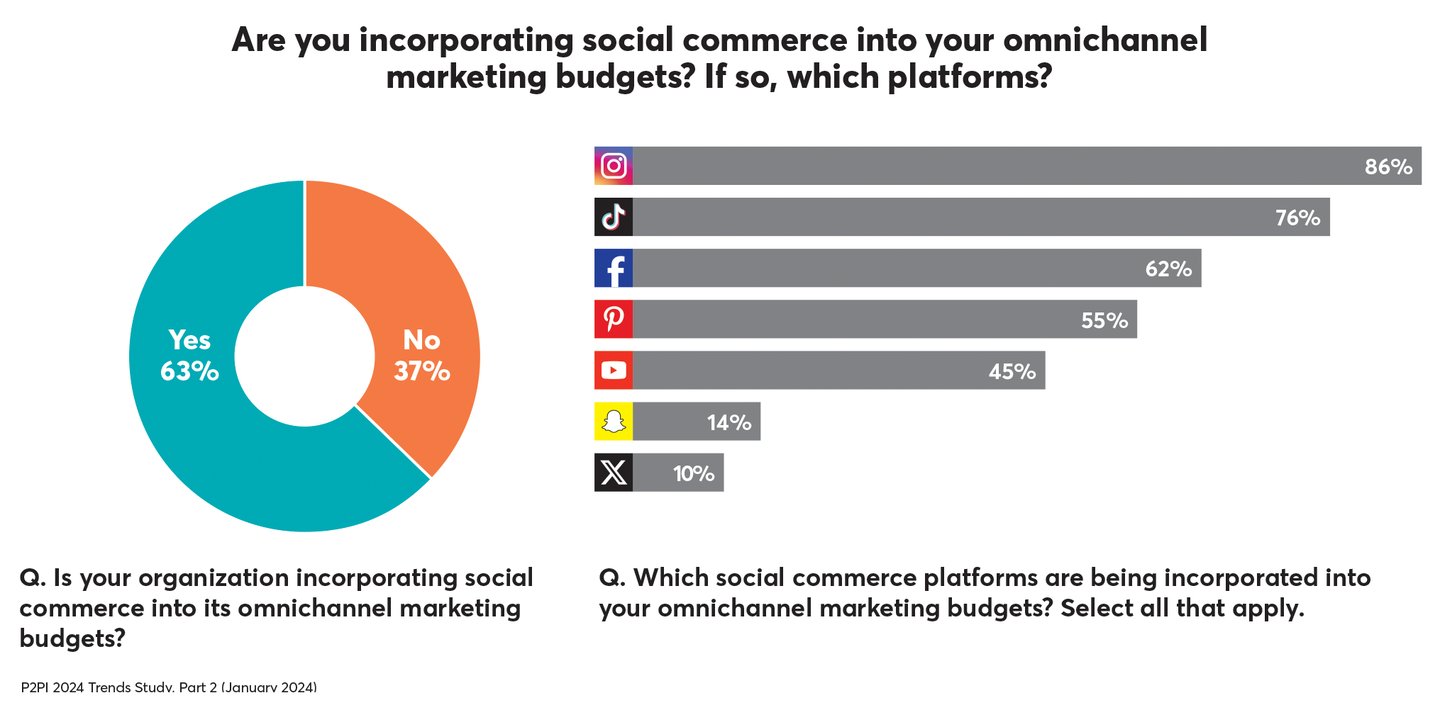

Later on in the survey, 63% of respondents said they were incorporating social commerce into their omnichannel marketing budgets, with Instagram (by 86%), TikTok (76%) and Facebook (62%) being identified as the most used platforms, and X (formerly known as Twitter) being named the least, just 10%.

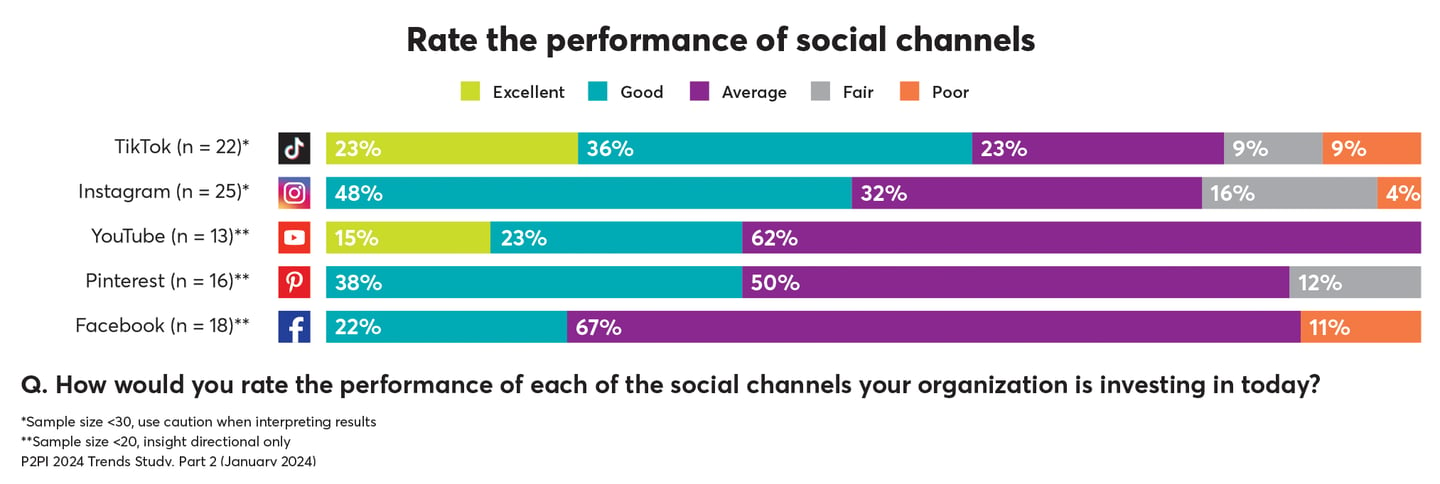

When the survey takers were asked to rate specific platforms’ performances, TikTok was rated excellent or good by 59%, and Instagram was rated good by 48% but excellent by none.

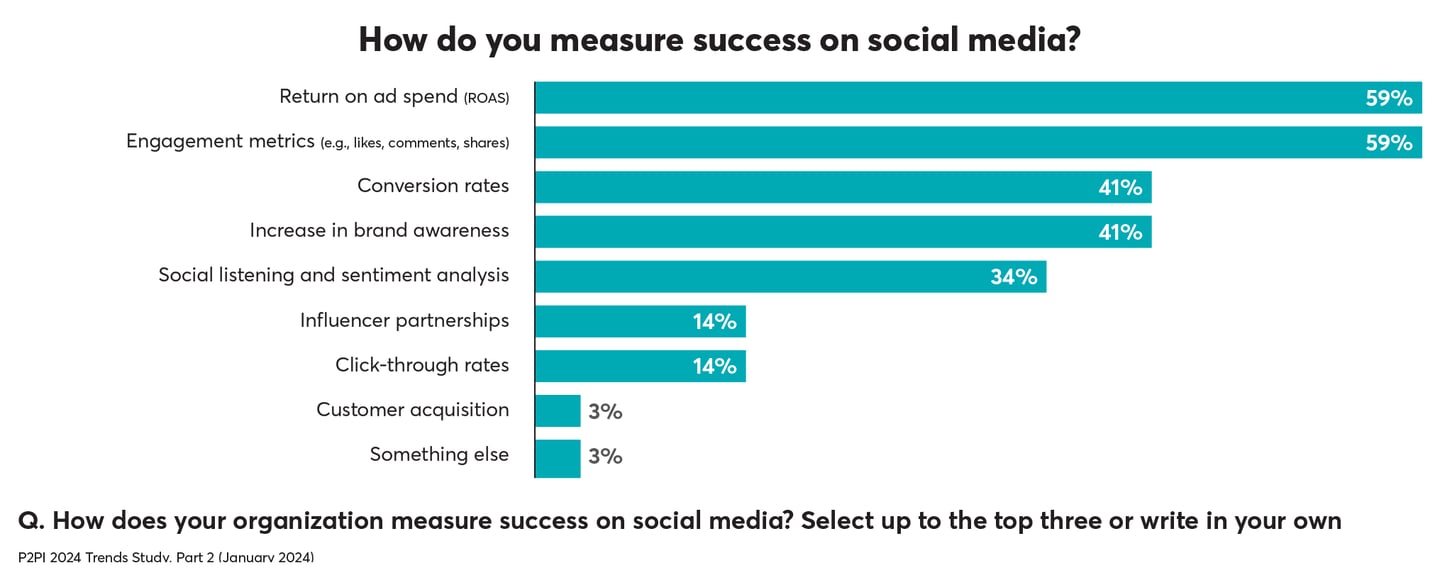

We then asked respondents to identify how they measured success on social media, choosing from our list of metrics. Return on ad spend (ROAS) and engagement metrics (likes, comments, shares) were named the most, each by 59%.

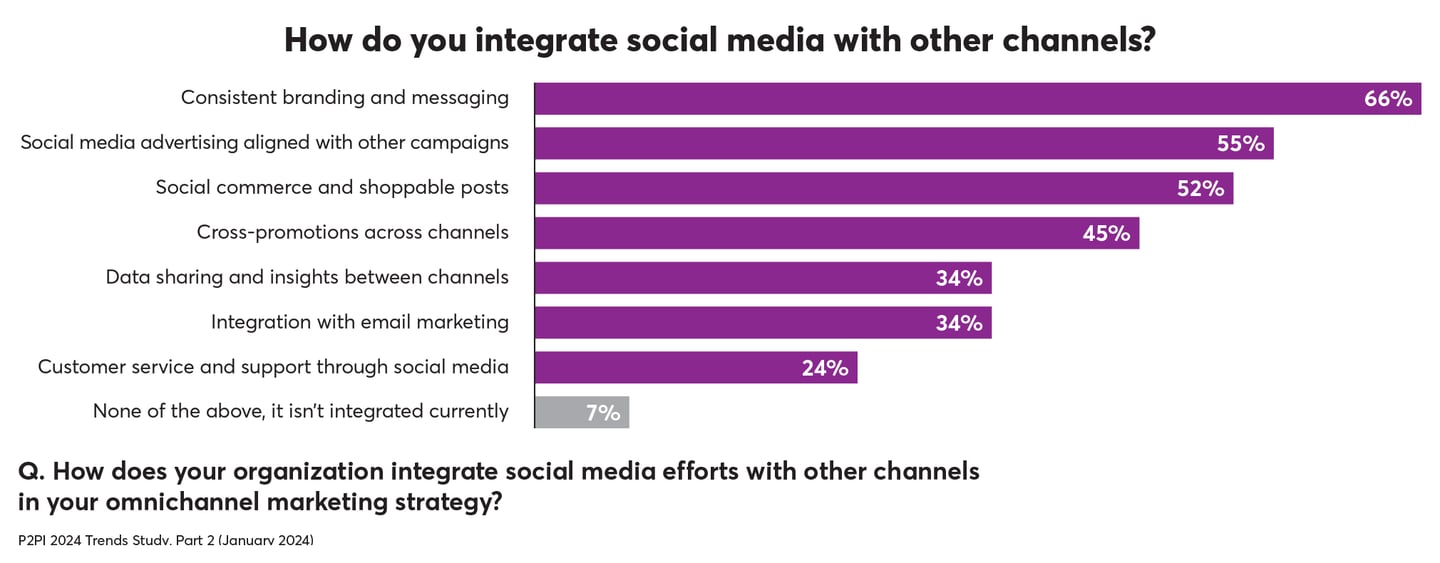

And in identifying how their organizations integrate their social media efforts with other marketing channels, respondents answered “consistent branding and messaging” (66%), “social media advertising aligned with other campaigns” (55%) and “social commerce shopping posts” (52%) most from our lists of answers.

Other Topics

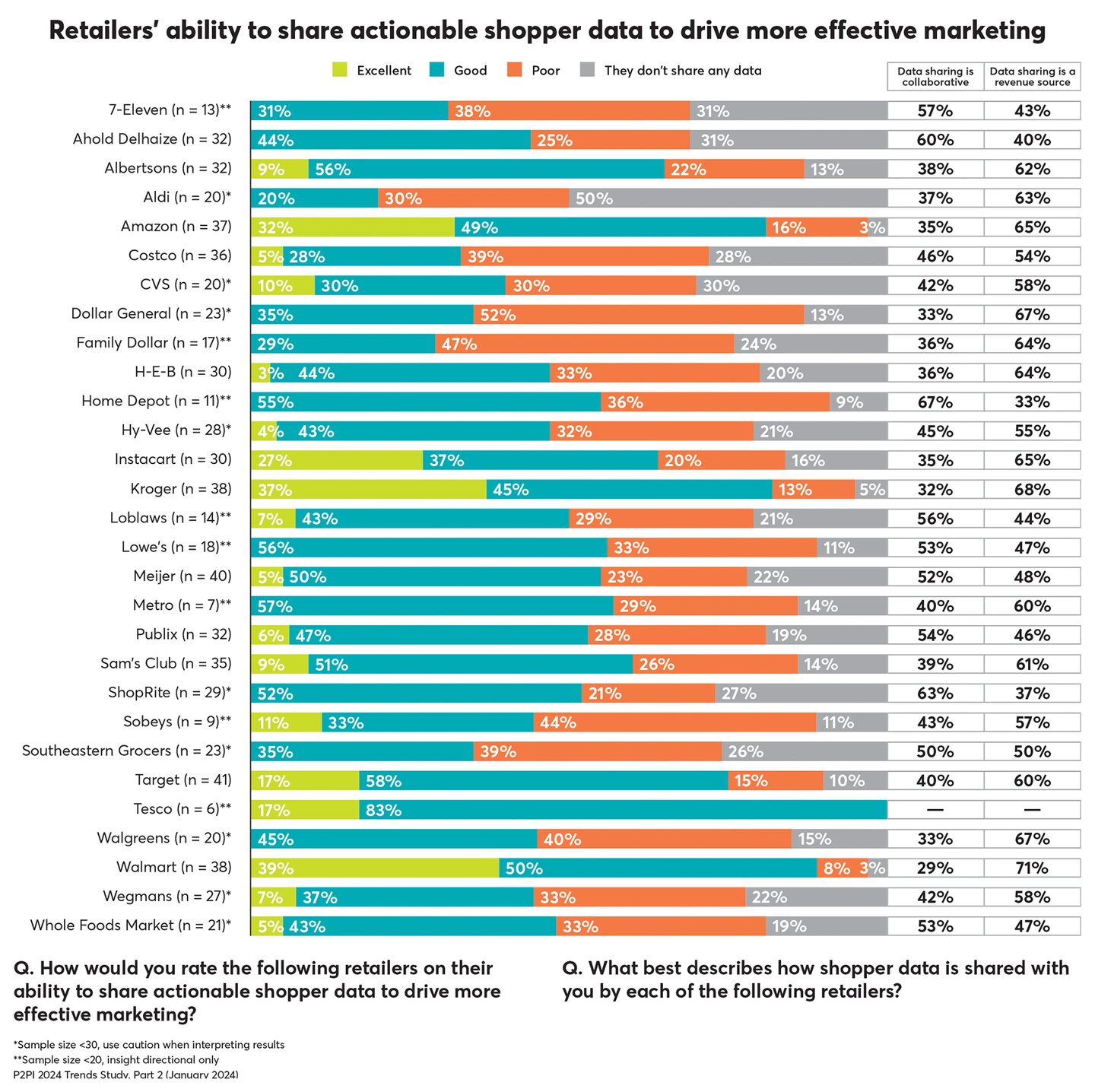

Retailer relationships. After identifying which retailers they’ve worked with in the last year, we asked respondents to rate those retailers on their ability to share actionable shopper data to drive more effective marketing. Walmart, Kroger, Amazon and Target were each identified as excellent or good by 75% of respondents who worked with them.

Meanwhile, ShopRite, 7-Eleven, Ahold Delhaize and The Home Depot were called out the most for their data sharing being collaborative, as opposed to a revenue source.

In-store tactics. From our list of tactics, “pricing and promotions” and a “true omnichannel approach” were identified by approximately half of respondents as what will most effectively drive shopper engagement inside the store going forward, followed by “innovative merchandising” (32%) and then “on-shelf signage” (21%).

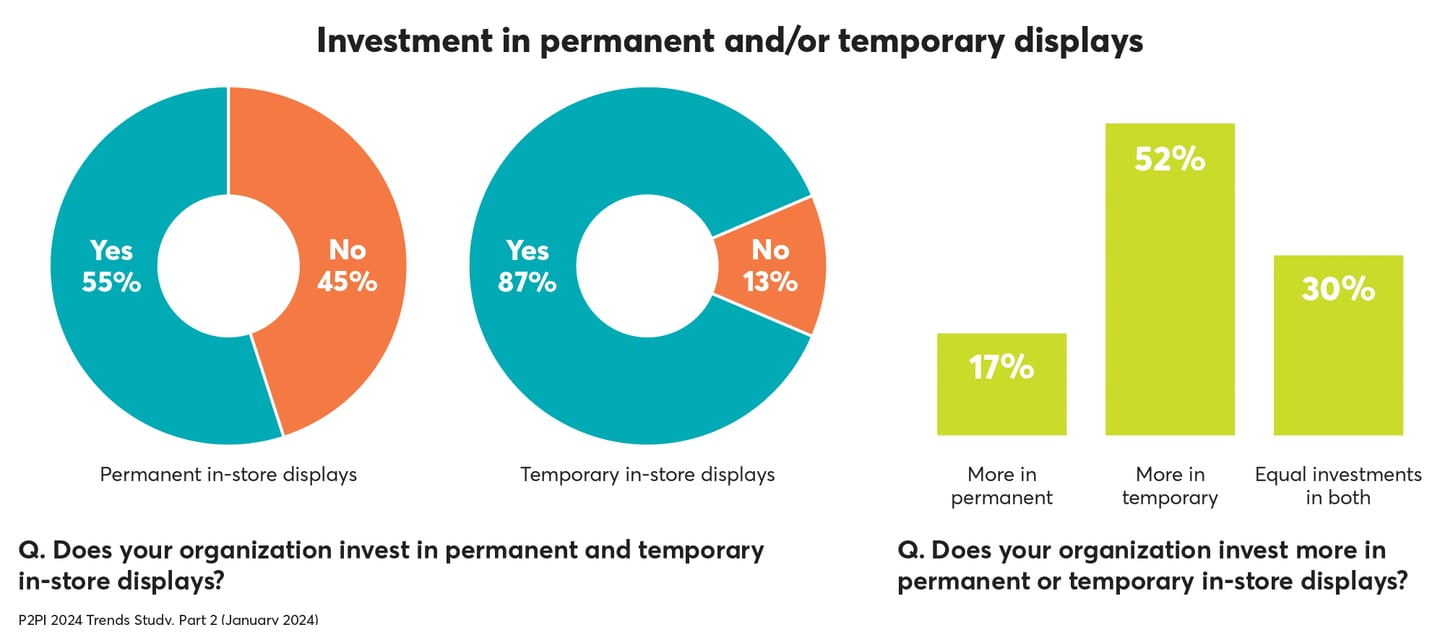

Furthermore, 55% of respondents said their organizations invest in permanent in-store displays, while 87% said they invest in temporary displays. Of respondents who said they invest in both, 52% said they invest more in temporary and 17% said they invest more in permanent.

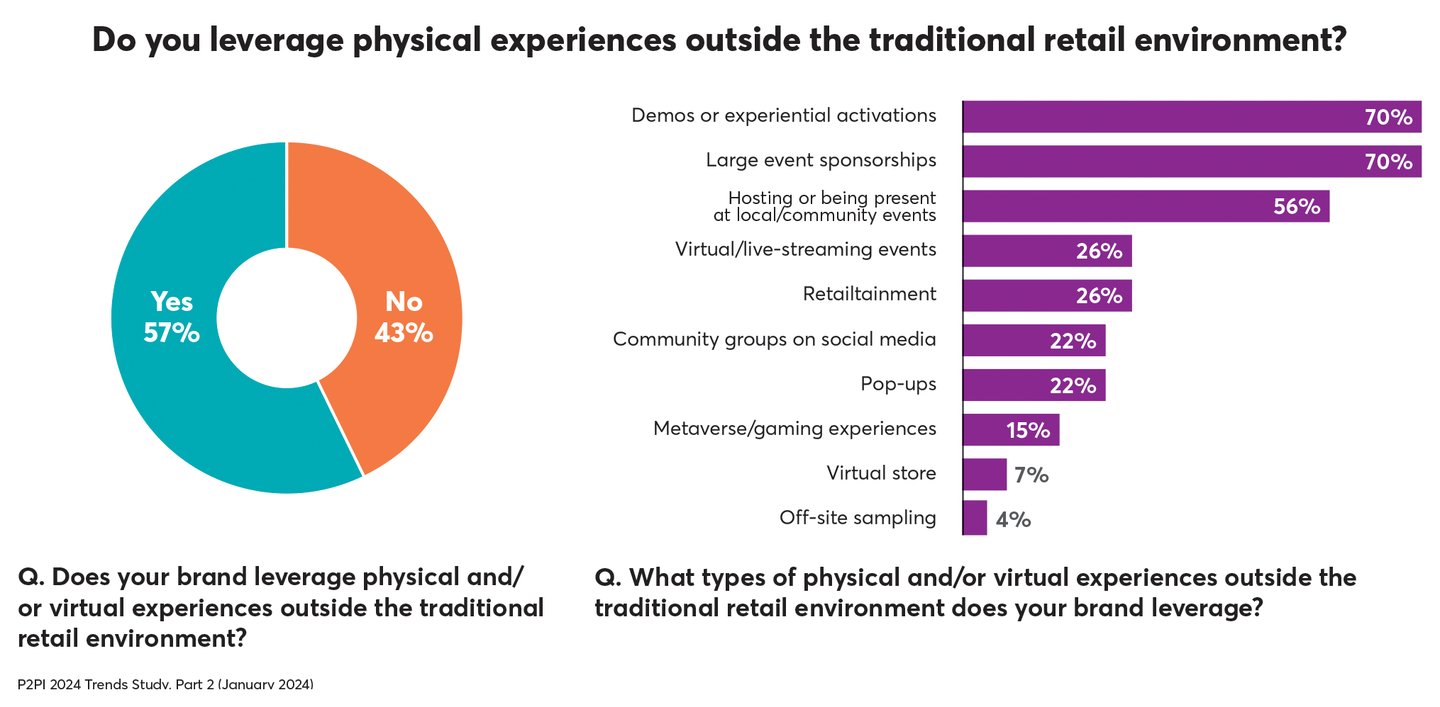

Experiences outside of traditional retail. Fifty-seven percent of respondents said they leverage physical and/or virtual experiences outside of retail, with “demos or experiential activations” and “large event sponsorships” (both 70%) being selected most from our list of options. Hosting or being present at local/community events followed at 56%.

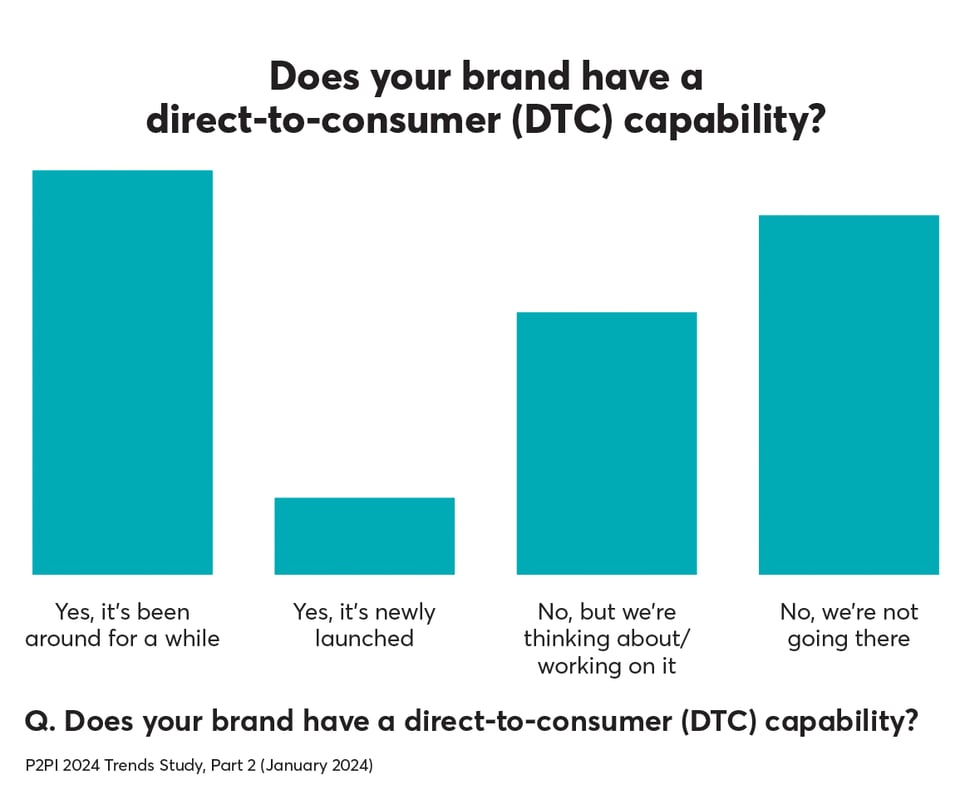

Direct to consumer. Forty-four percent of our survey takers said their brands have a DTC capability, while 24% said they didn’t but were working on it or thinking about it. Thirty-three percent said their brands weren’t going there.

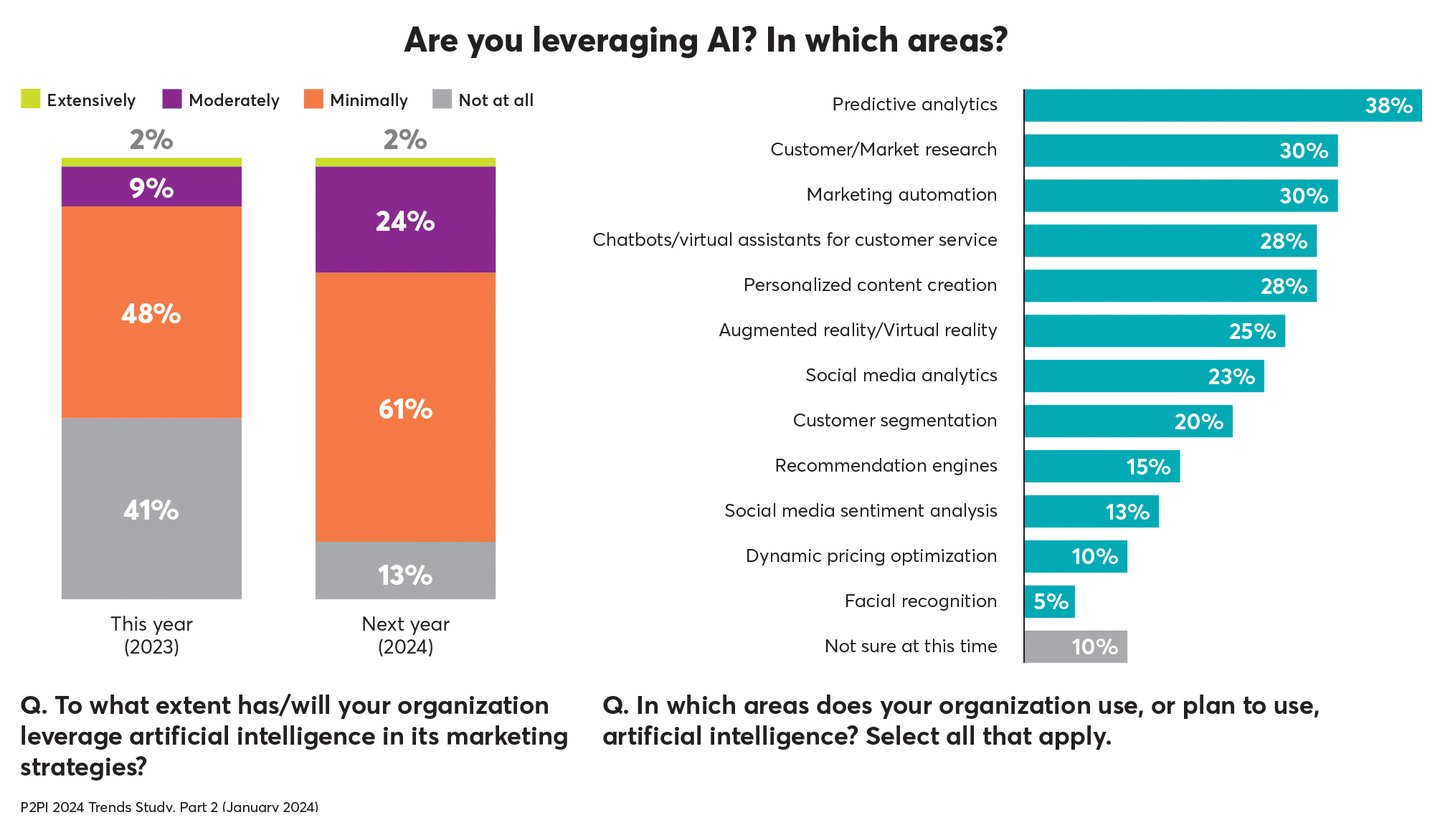

Artificial intelligence. Fifty-nine percent of respondents said their organizations were already leveraging AI in their 2023 marketing strategies — 48% qualified their use as minimal and 11% as moderate or extensive. For 2024, 87% said they will leverage it — 61% minimally and 26% moderately or extensively.

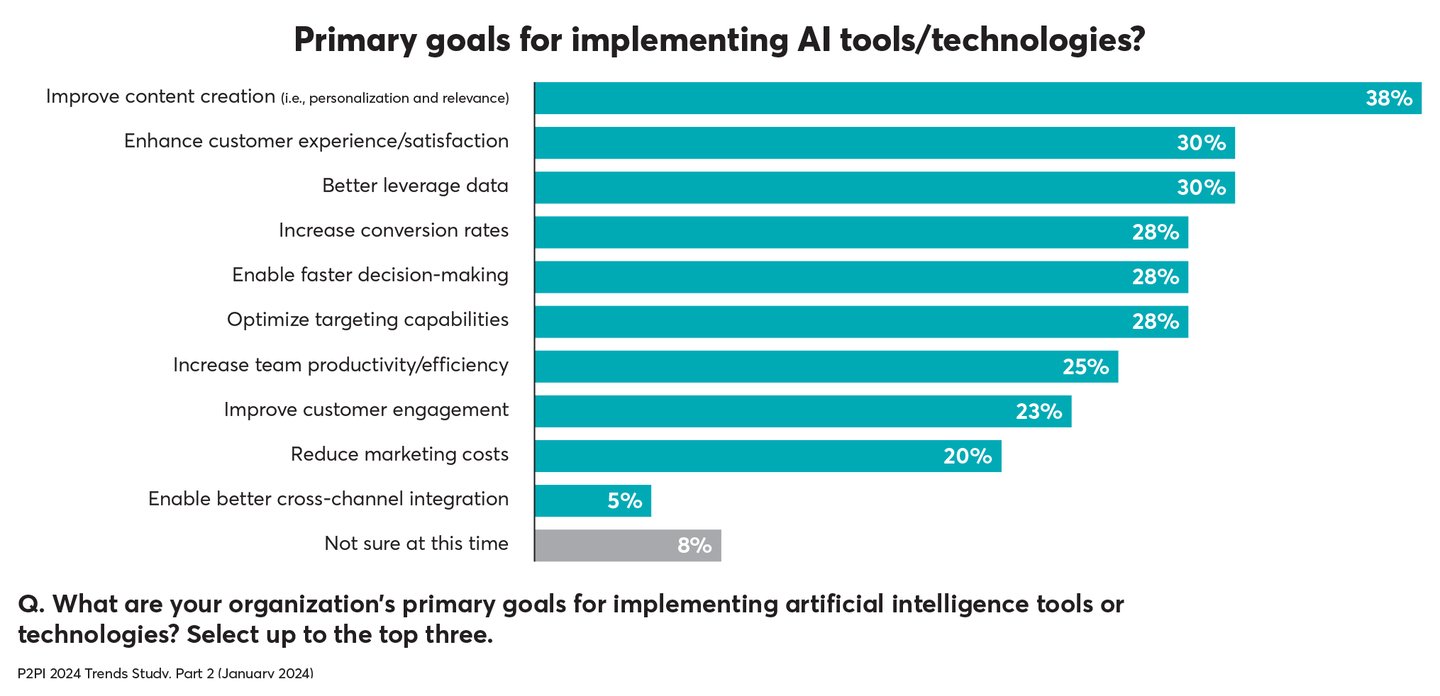

And asked what their organization’s primary goals were for implementing AI tools or technologies, 38% selected “improve content creation” from our list of goals. Eight other goals were selected by at least 20% of respondents, with “better leverage data” and “enhance customer experience/satisfaction” ranking second and third overall.