Trends 2024, Part 1: Retailer Media Network Ratings & Insights

Retail media — and all its opportunities and challenges — has been a strong focus at the Path to Purchase Institute for the past several years. Retail media’s growth and impact on the commerce marketing world has been unbelievable and unrelenting, and Insider Intelligence has forecasted U.S. retail media ad spend to more than double between 2023 and 2027 from $46 billion to $109 billion.

While the numbers that surround retail media are big and get thrown around a lot now, let’s think back to what helped steer our attention toward the growing retail media opportunity several years back: our annual Trends survey.

Since 1995, the Path to Purchase Institute has conducted a yearly Trends survey to examine the major issues affecting consumer goods companies. To devise the survey questions, our editorial team comes together every fall to discuss hot topics and trends gleaned from our reporting, educational events and webinars, as well as conversations with CPG brand professionals, retailers, solution providers and agencies.

It was clear to us years ago that our commerce community was eager to learn more about retailer media networks (RMNs) and related companies, including their impact on the omnichannel landscape. Recognizing these insights, we’ve made sure to include several questions related to retail media in our survey over the past five years, as well as a section devoted to rating RMNs. Furthermore, the retail media portion of the survey has grown so large that we decided to split our report into two parts, with the first dedicated to retail media. (We will report on Part 2 in our March/April issue.)

For the retail media portion of this year’s report, we surveyed 76 CPG brand professionals between Sept. 18 and Oct. 10, 2023. To qualify for the survey, respondents had to indicate they worked with one or more retailer media networks. A majority of respondents surveyed (53%) were managers, followed by directors (41%) and senior management (6%). When it came to their primary job functions, 38% of survey takers indicated shopper marketing, while the rest varied from retail media (13%) to e-commerce (11%). A third reported working with packaged food and snack items, followed by other categories including packaged household items (16%), non-alcoholic beverages (12%), over-the-counter drugs/medical (7%), beer/wine/liquor (5%) and confectionery (5%).

Investments and Budget Allocations

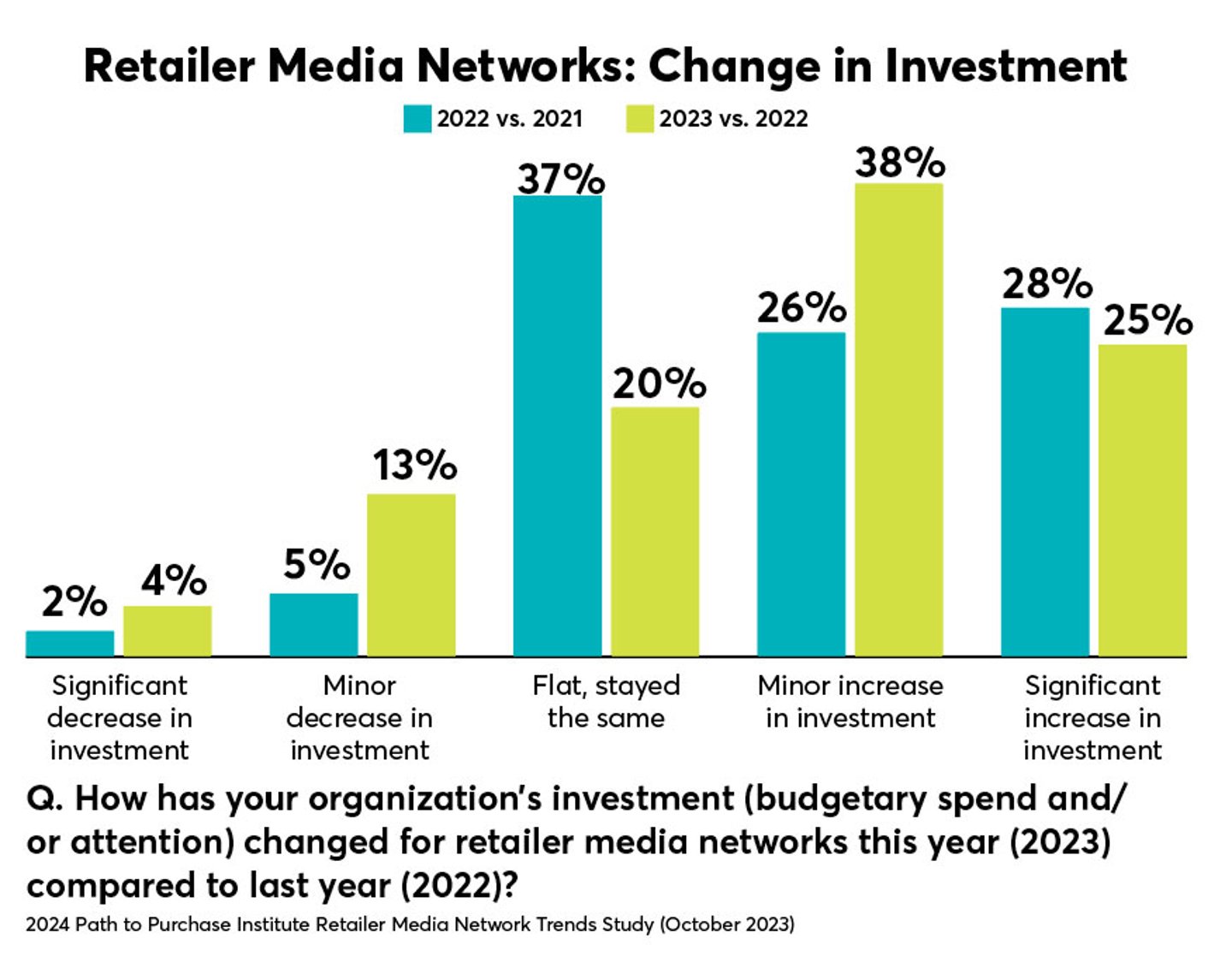

Considering the retail media industry forecasts, it will come as no surprise that more than 3-in-5 respondents indicated that their CPG organizations increased spending in retailer media networks in 2023. Sixty-three percent of respondents reported at least a minor increase in retail media investment at their companies compared to 2022, which is a slight increase from last year’s Trends report, when 53% reported a minor increase in 2022 compared to 2021.

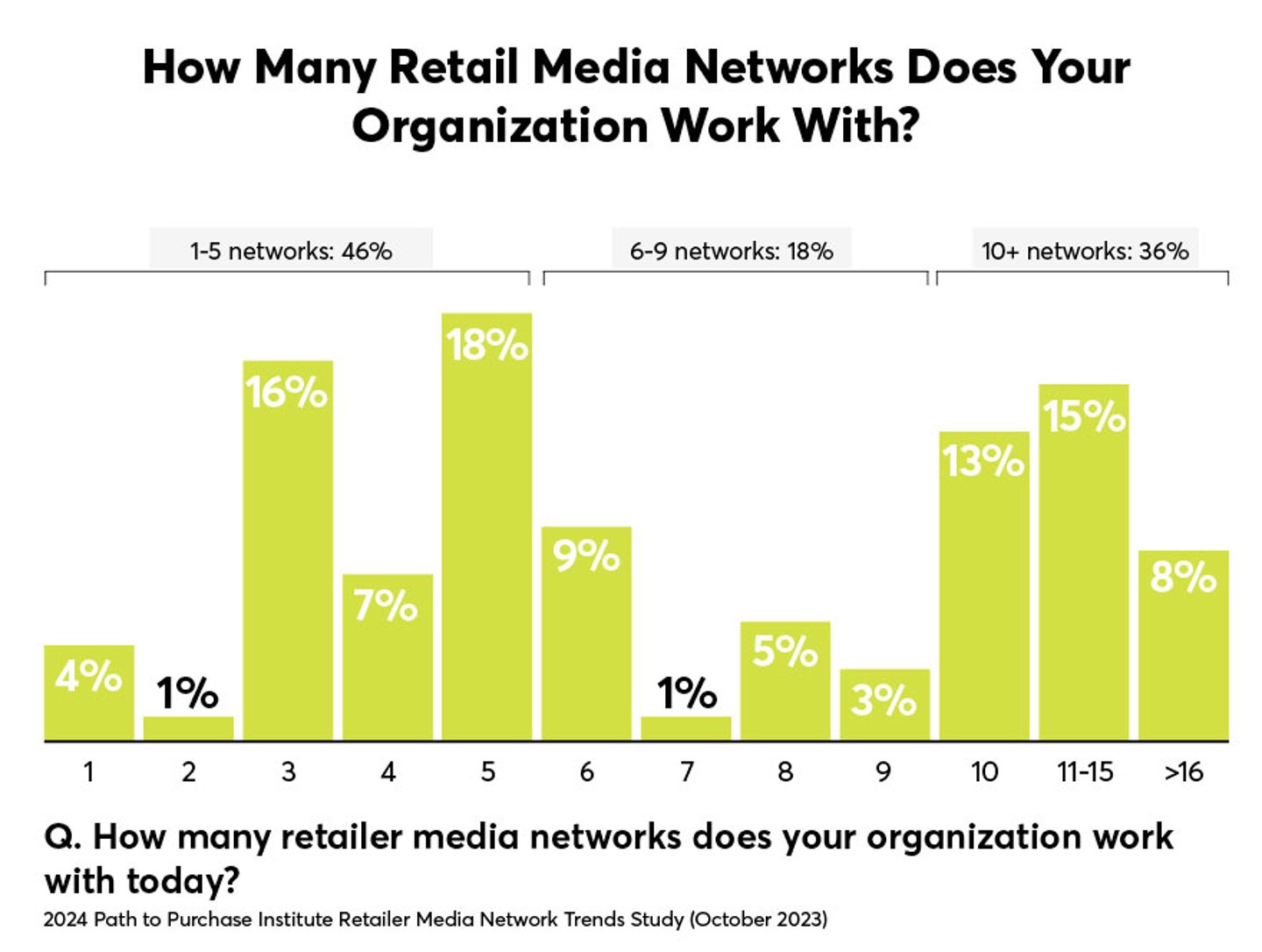

What is staggering, however, is the number of RMNs CPG brand manufacturers are currently juggling. Half of survey takers told us their organizations are currently working with three to six RMNs, while 36% said they’re working with 10 or more. For comparison, we asked the same question in a research study in the summer of 2022 and only 6% of CPG brand survey takers indicated working with more than 10 networks.

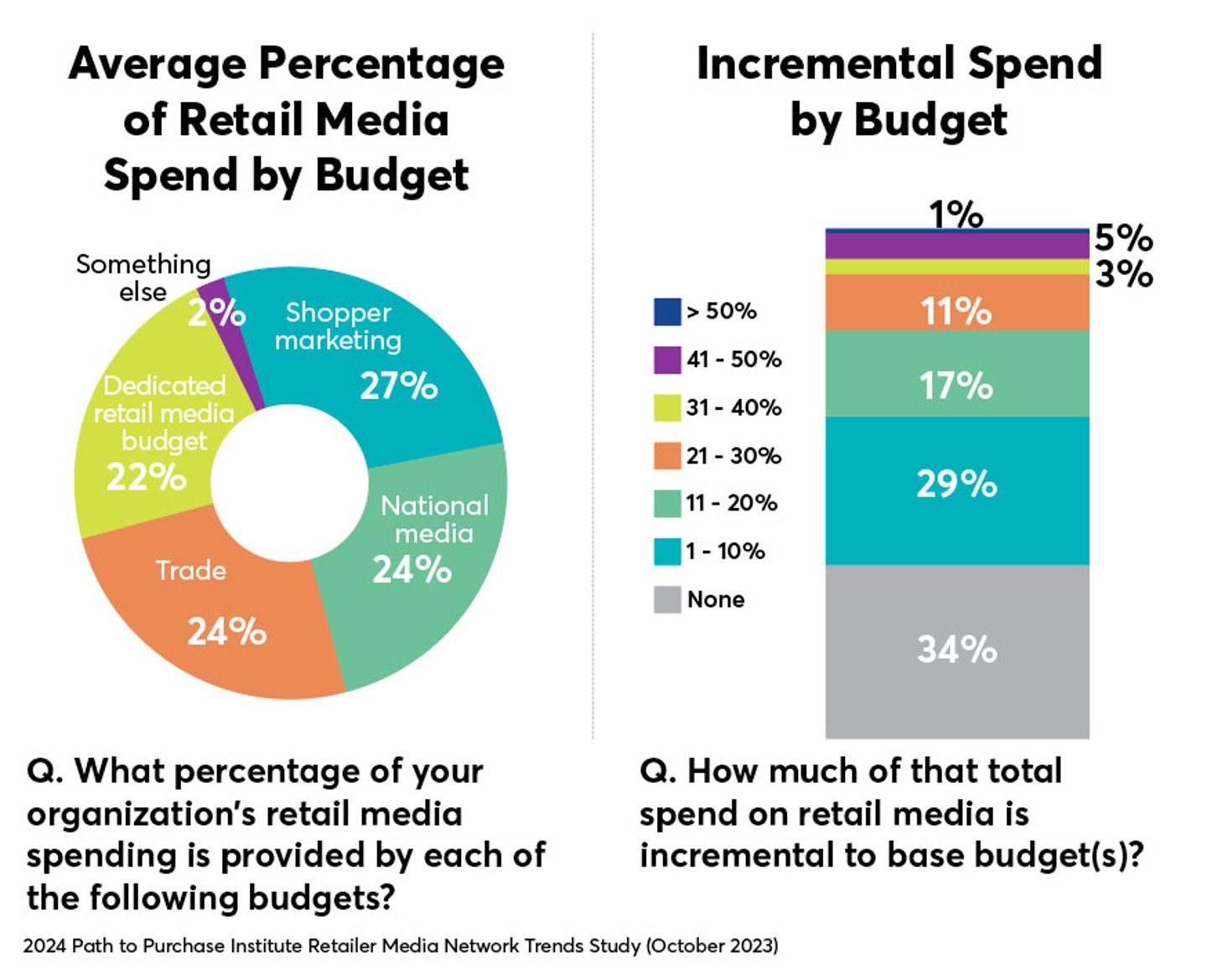

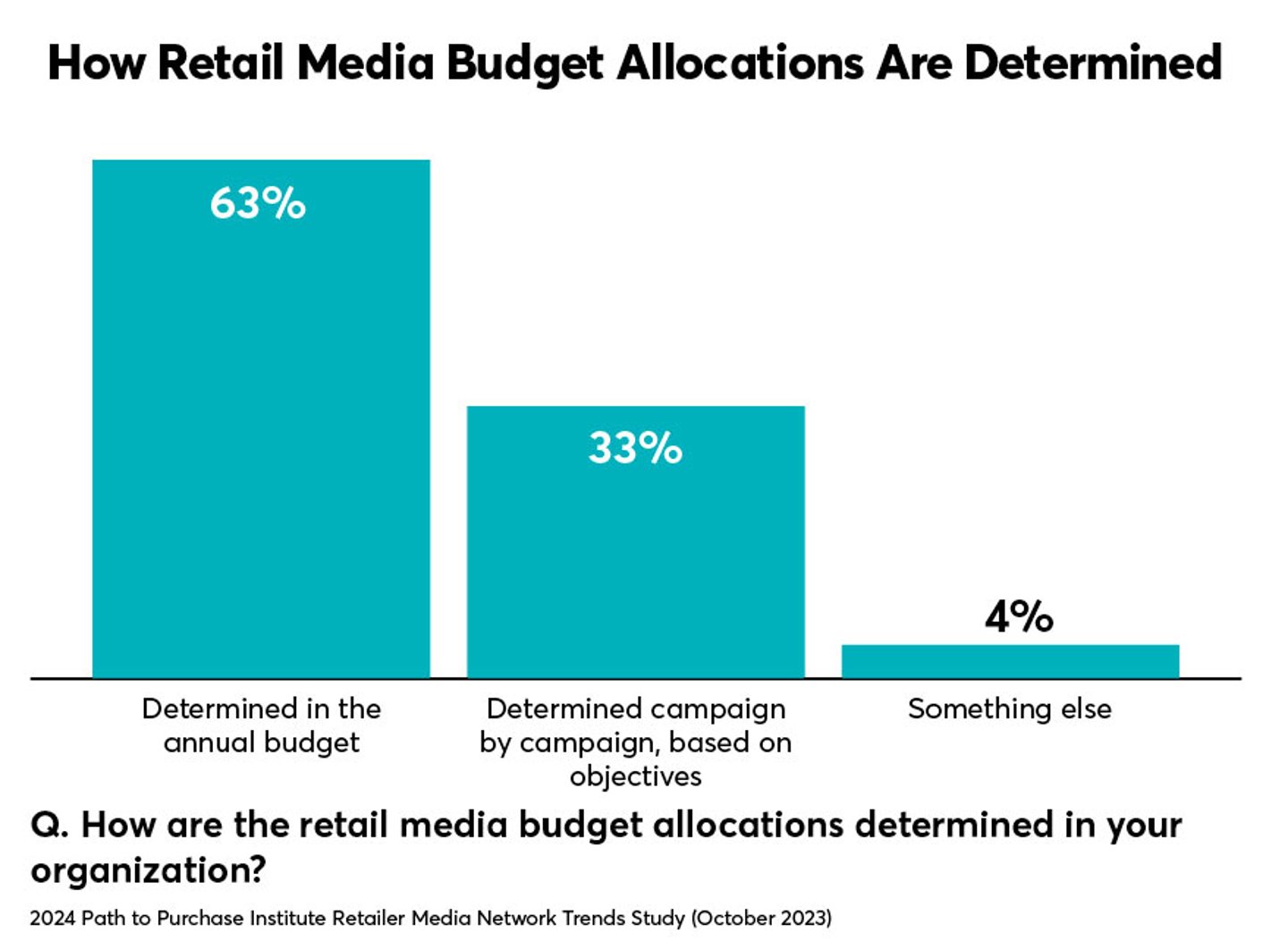

Looking at budget allocations, we found that retail media spending is coming from a variety of these marketing budgets. Shopper marketing budgets are most commonly used to fund retail media efforts, followed relatively closely by national media, trade and a dedicated retail media budget. When we asked how retail media budget allocations are determined in their organization, 63% of respondents said they were determined in an annual budget, while a third reported they were determined campaign by campaign based on objectives.

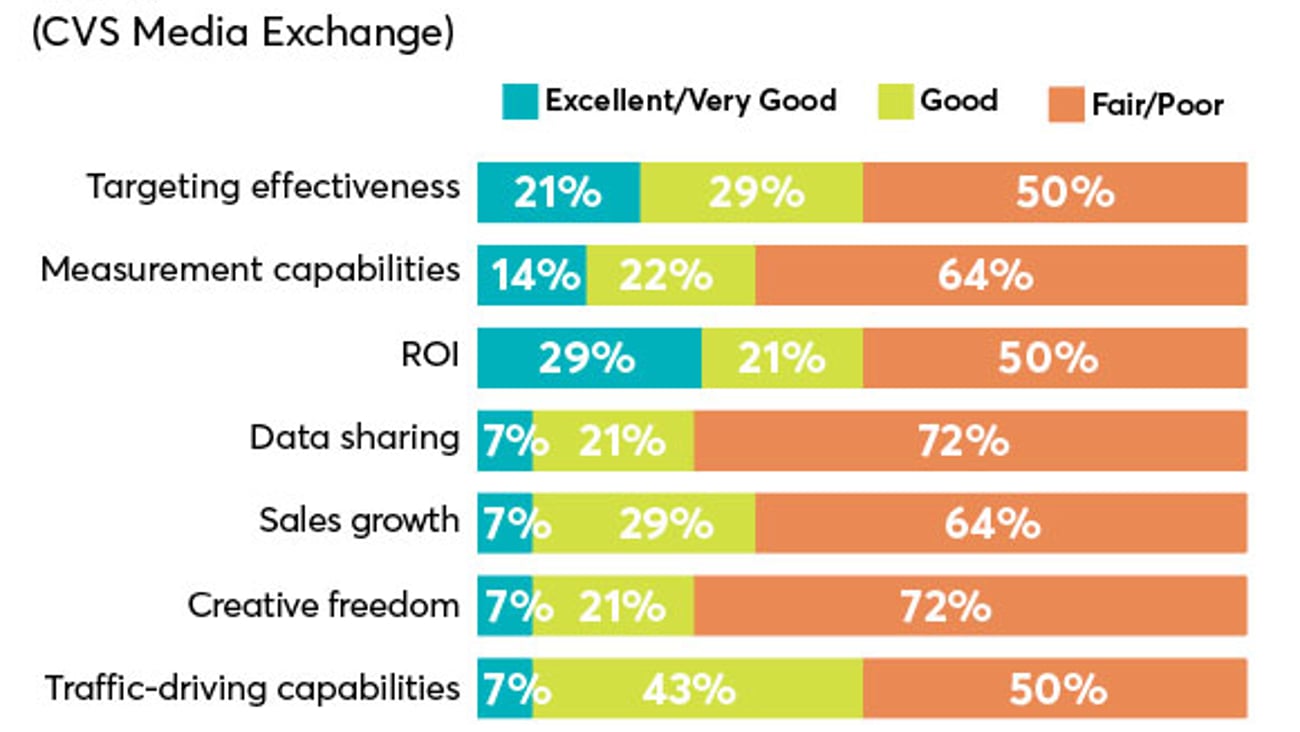

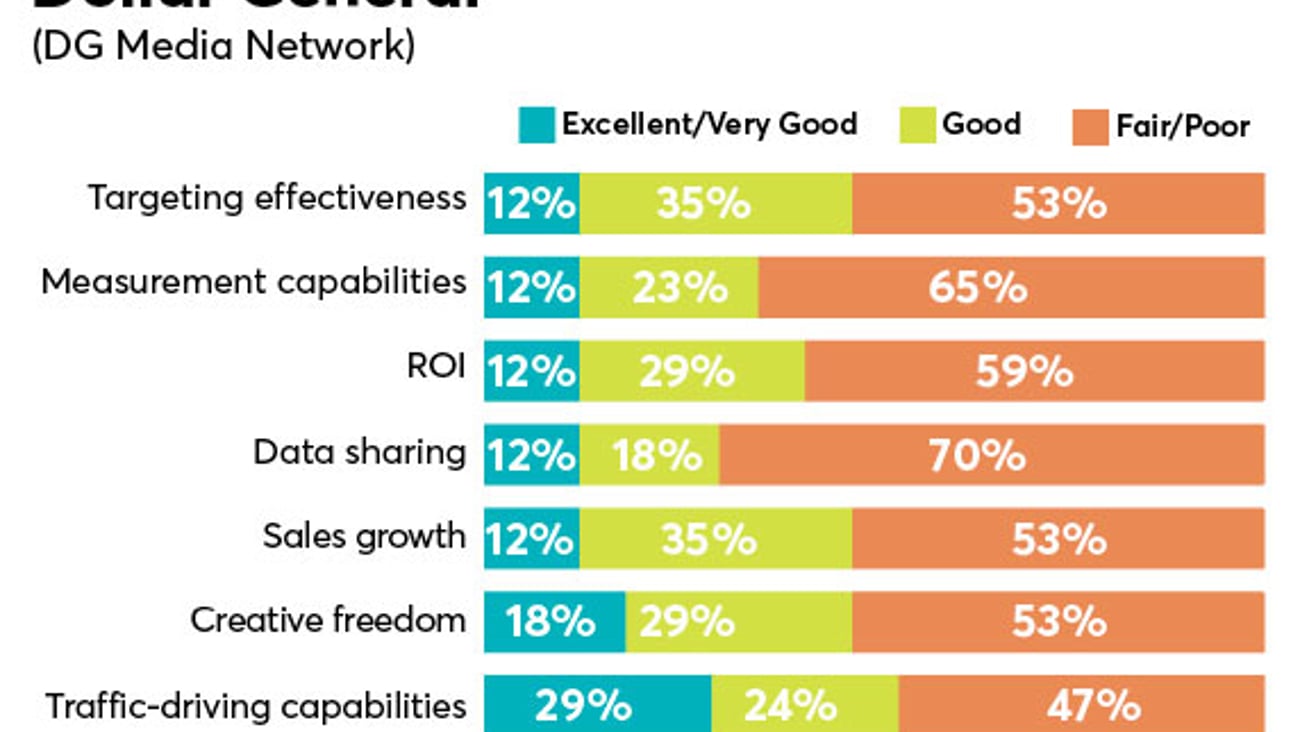

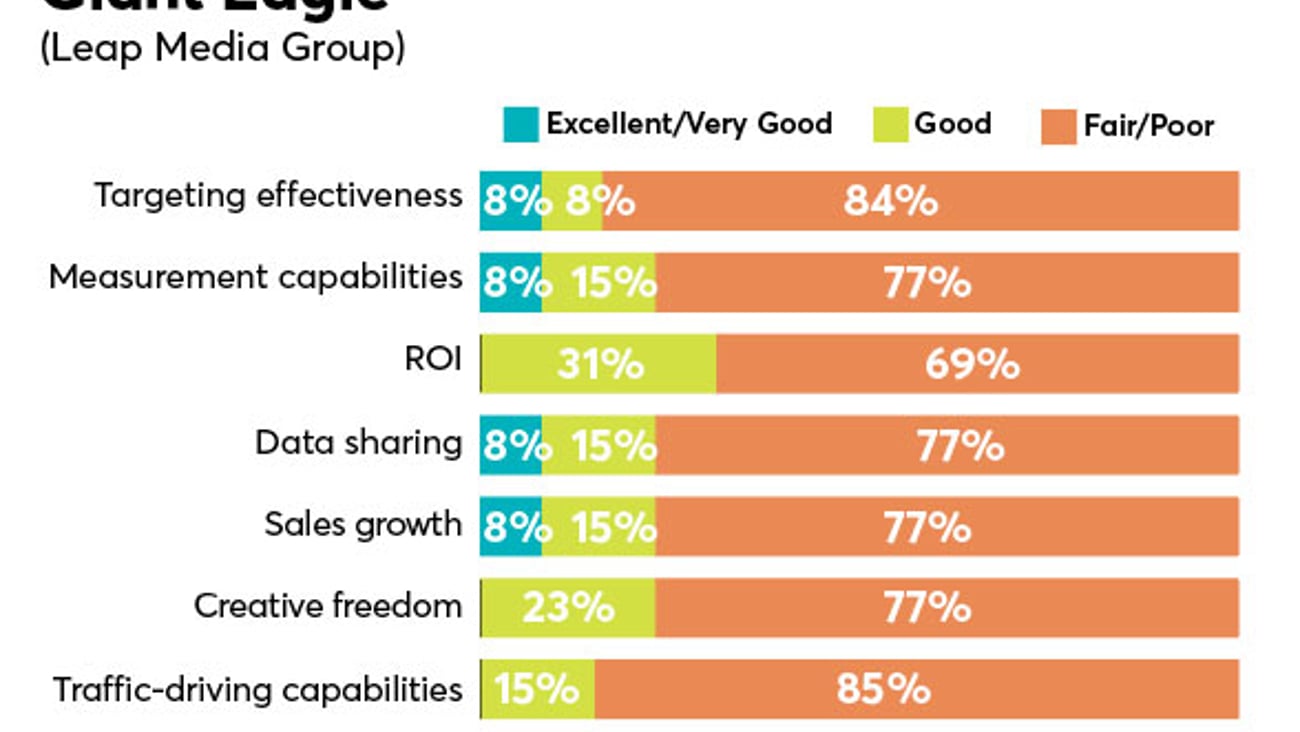

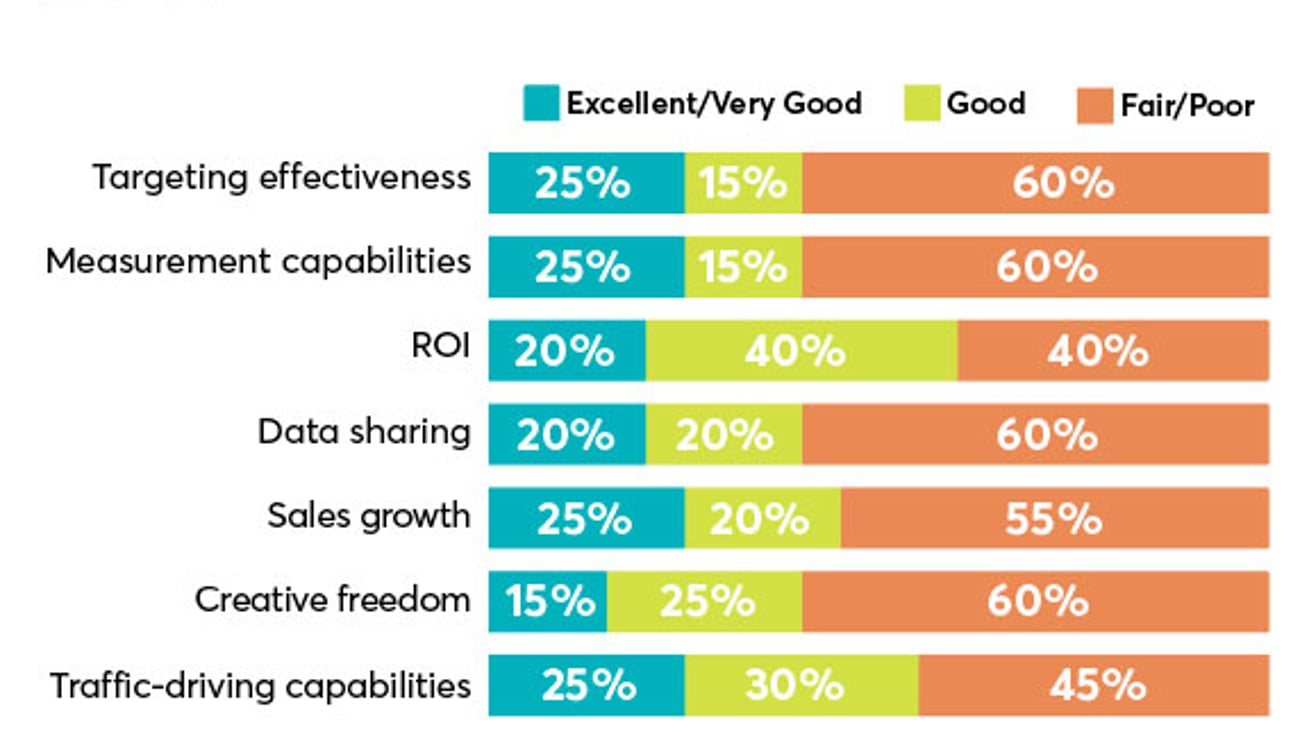

Retailer Media Network Ratings

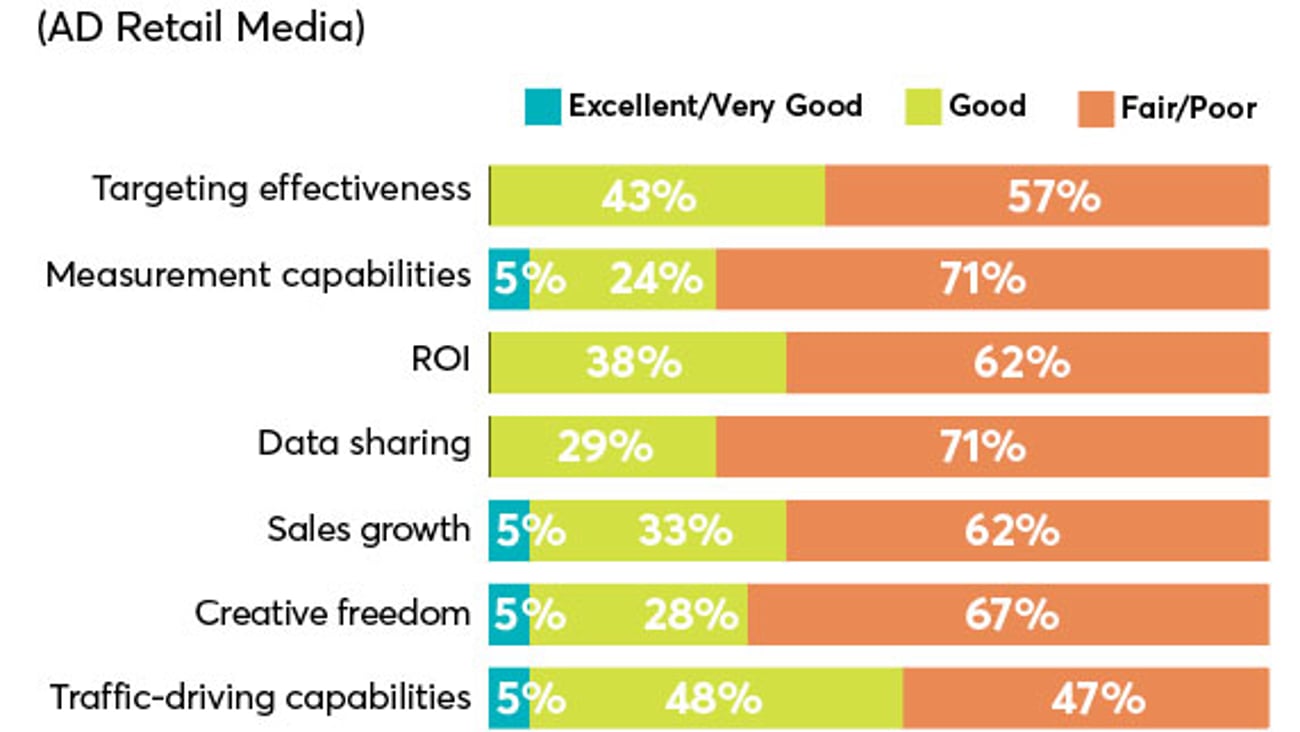

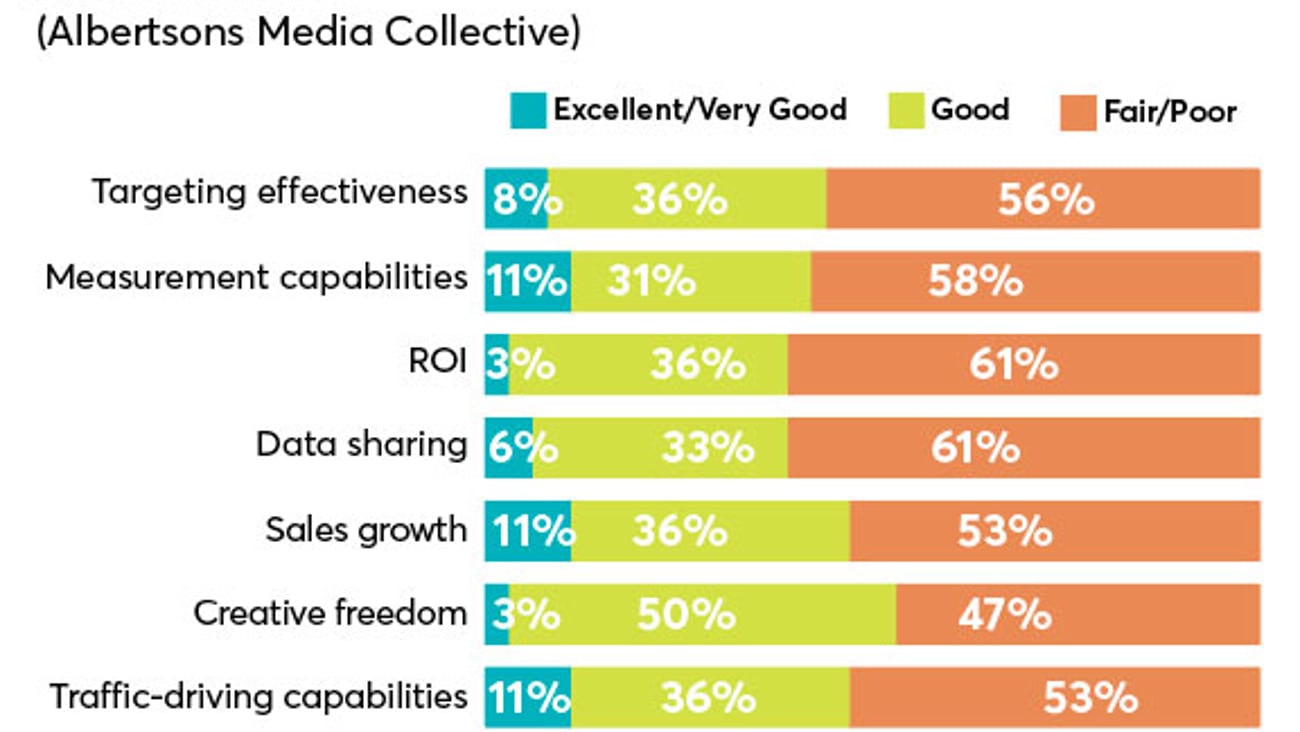

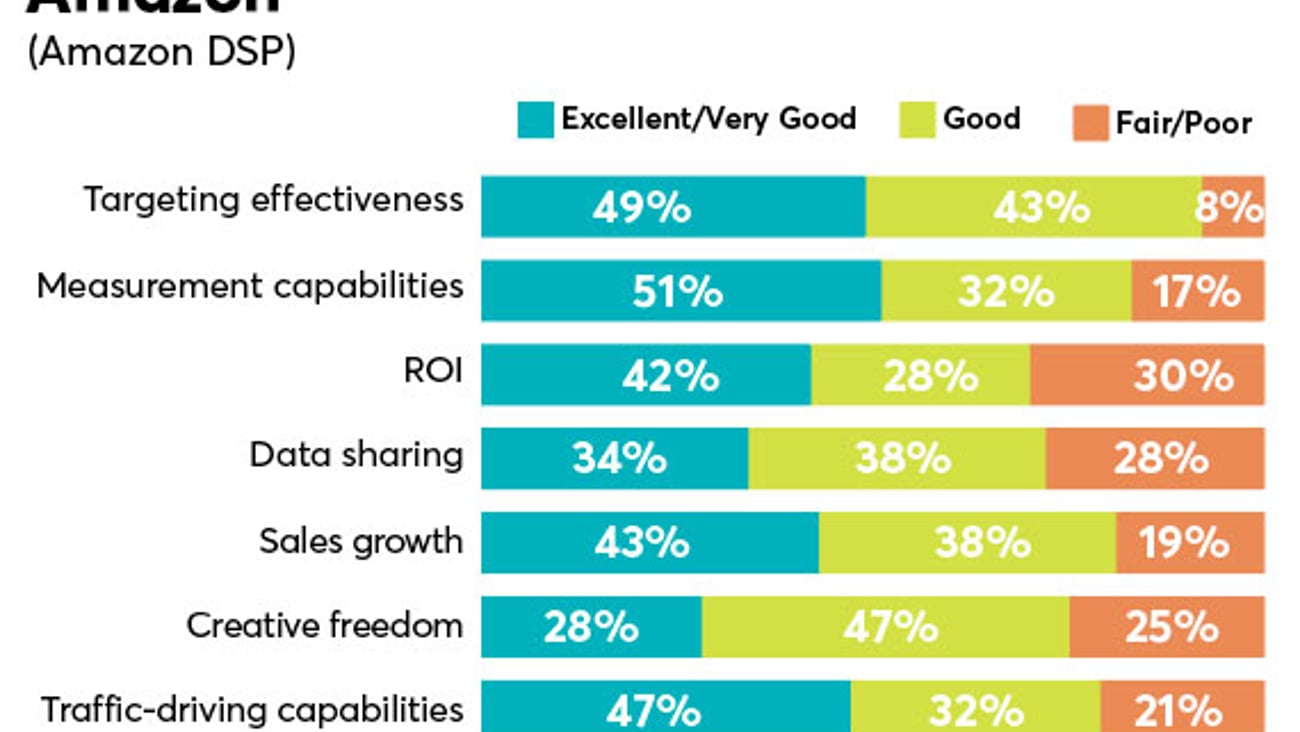

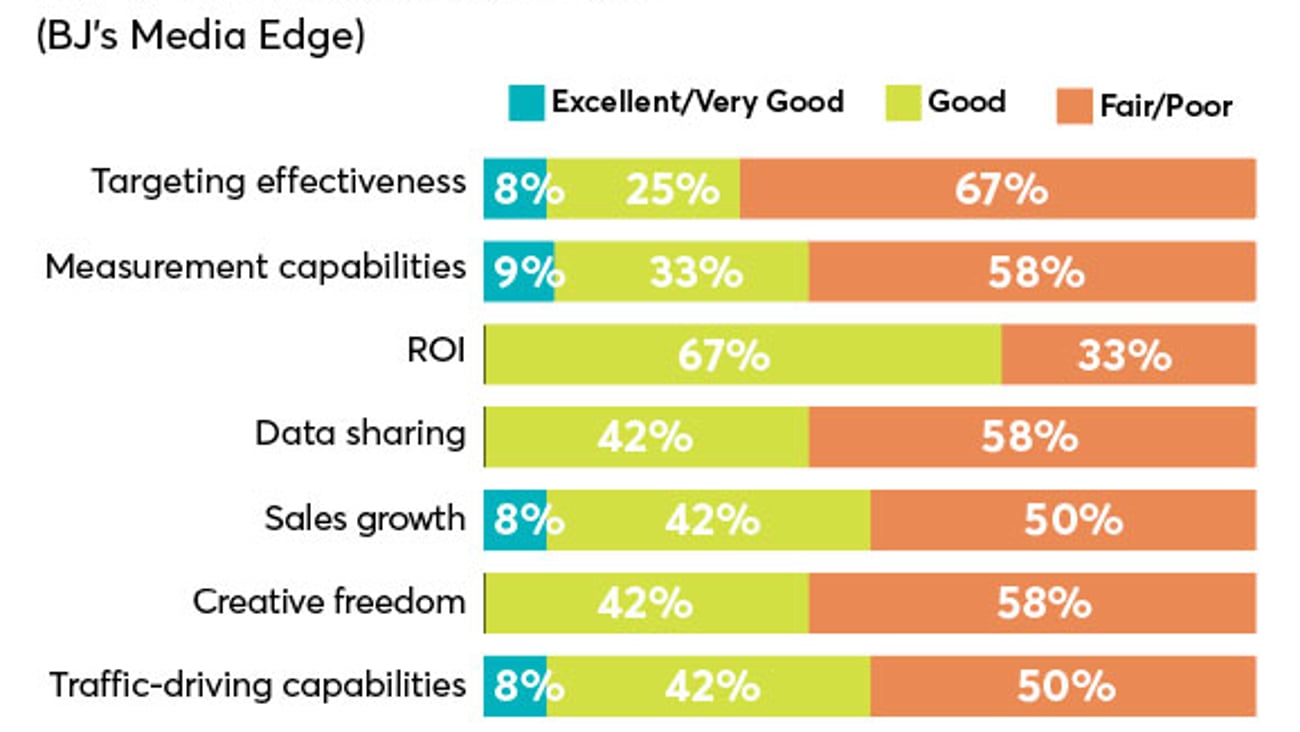

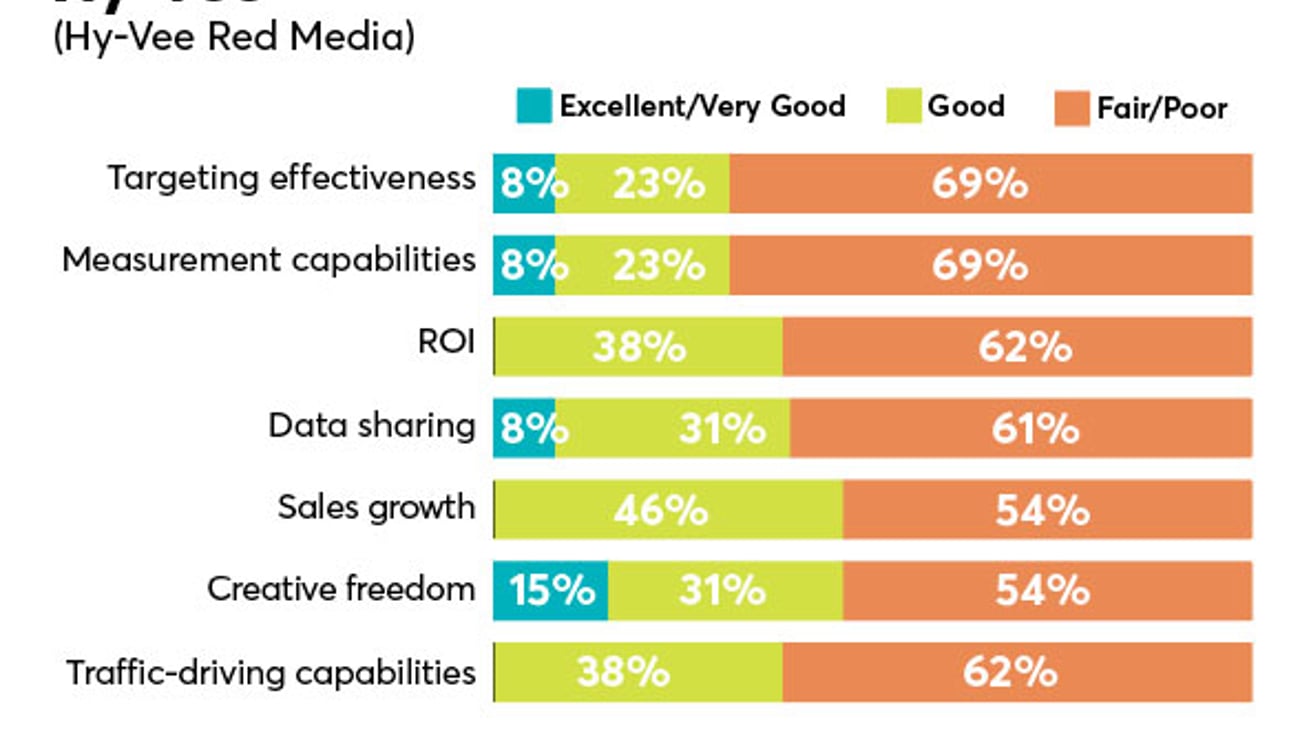

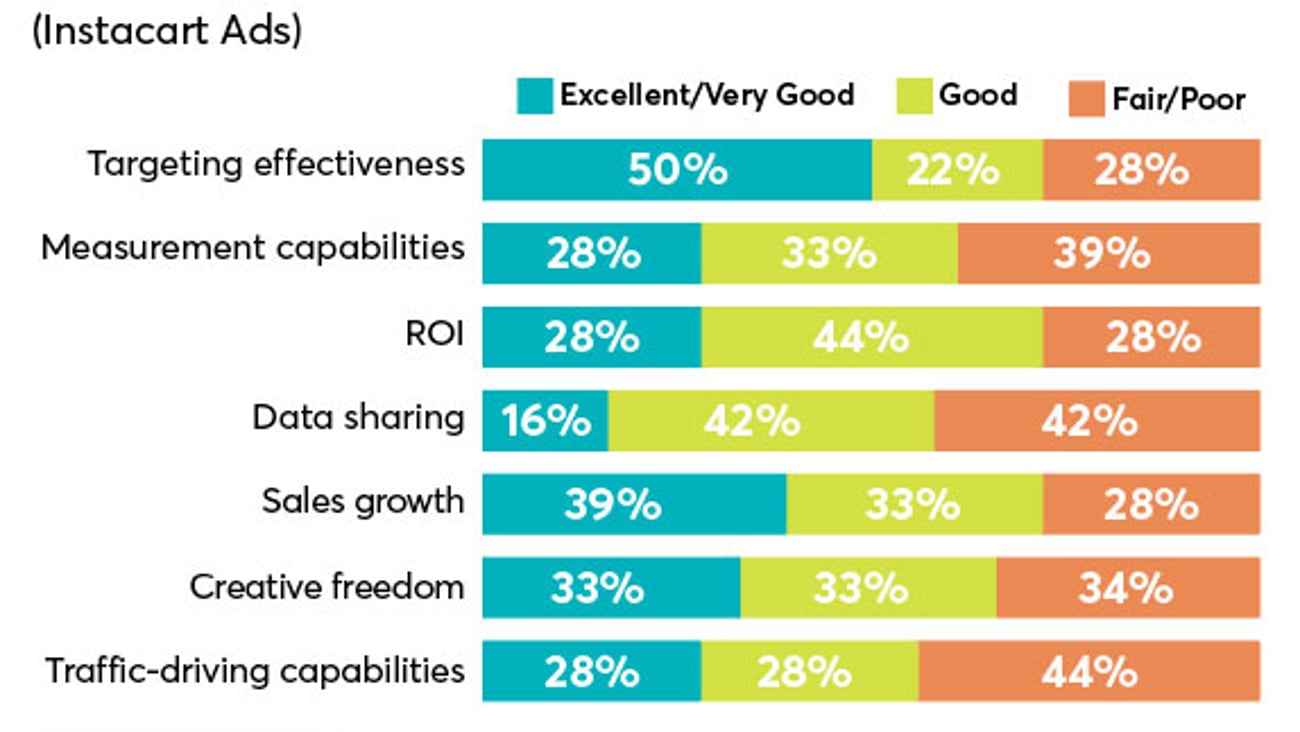

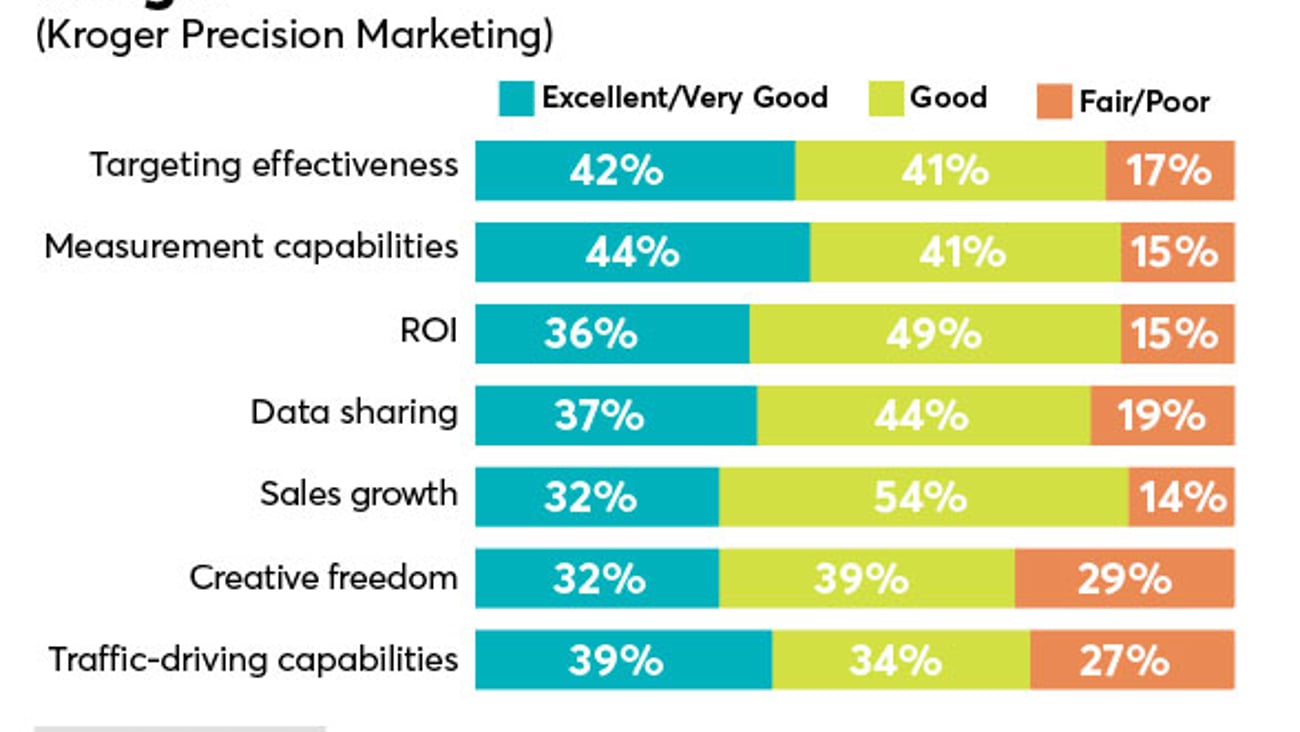

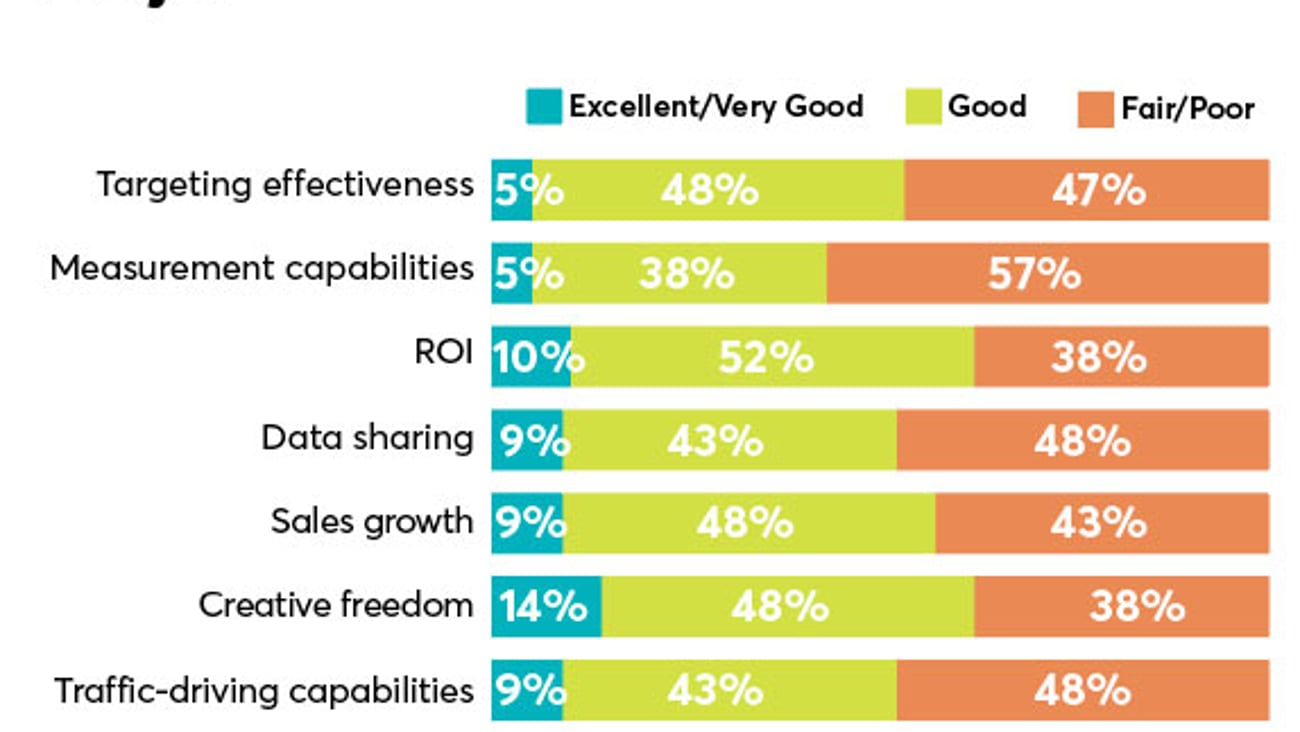

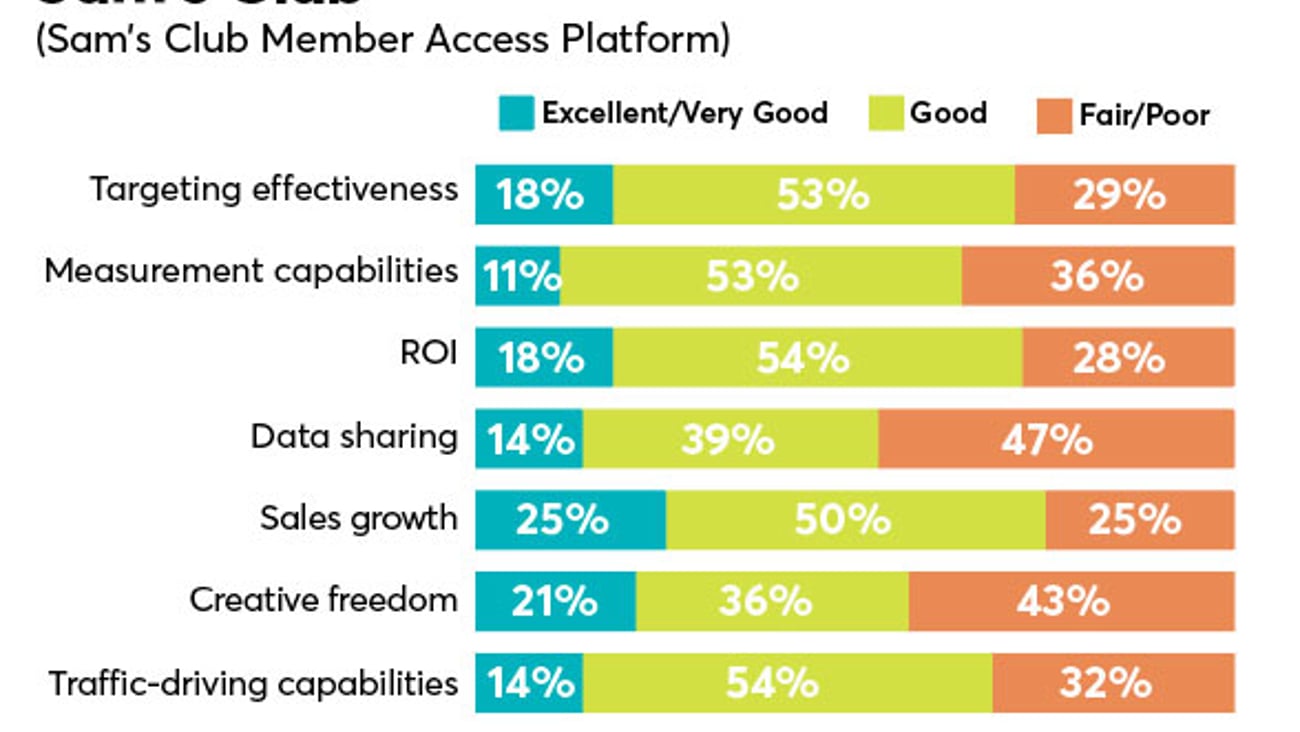

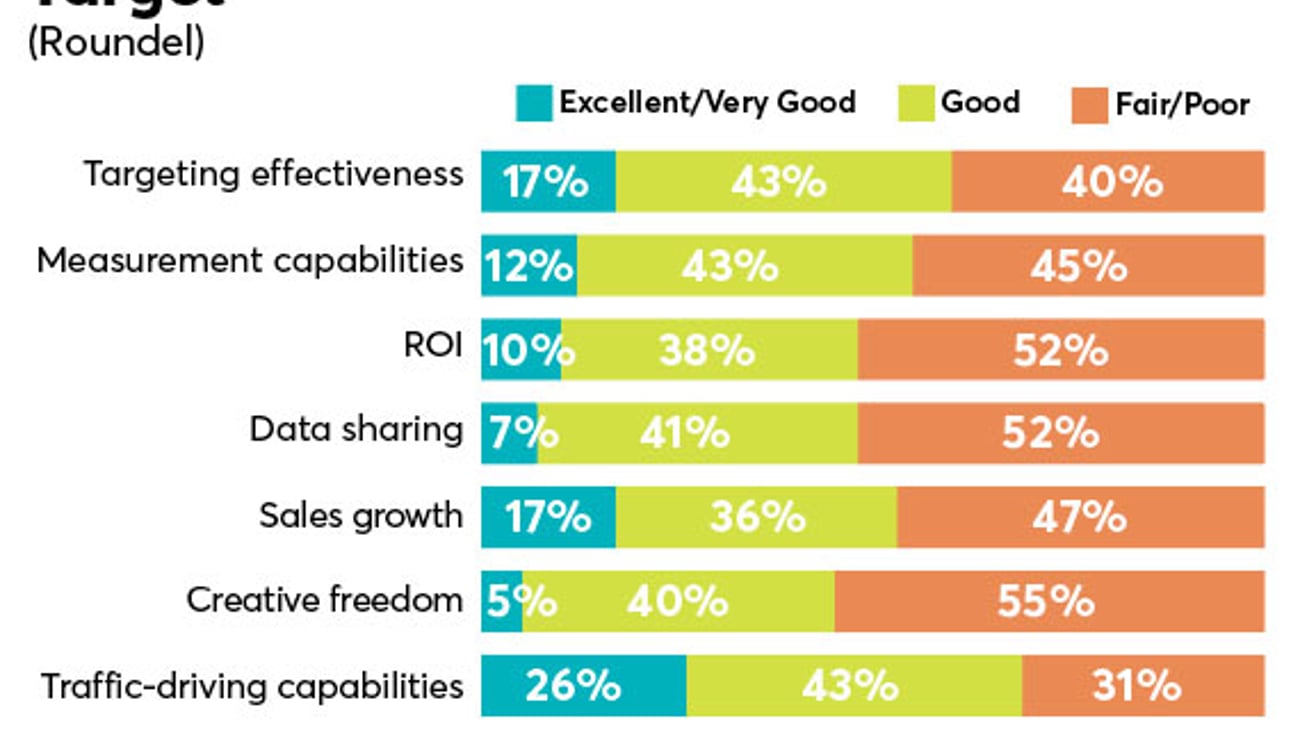

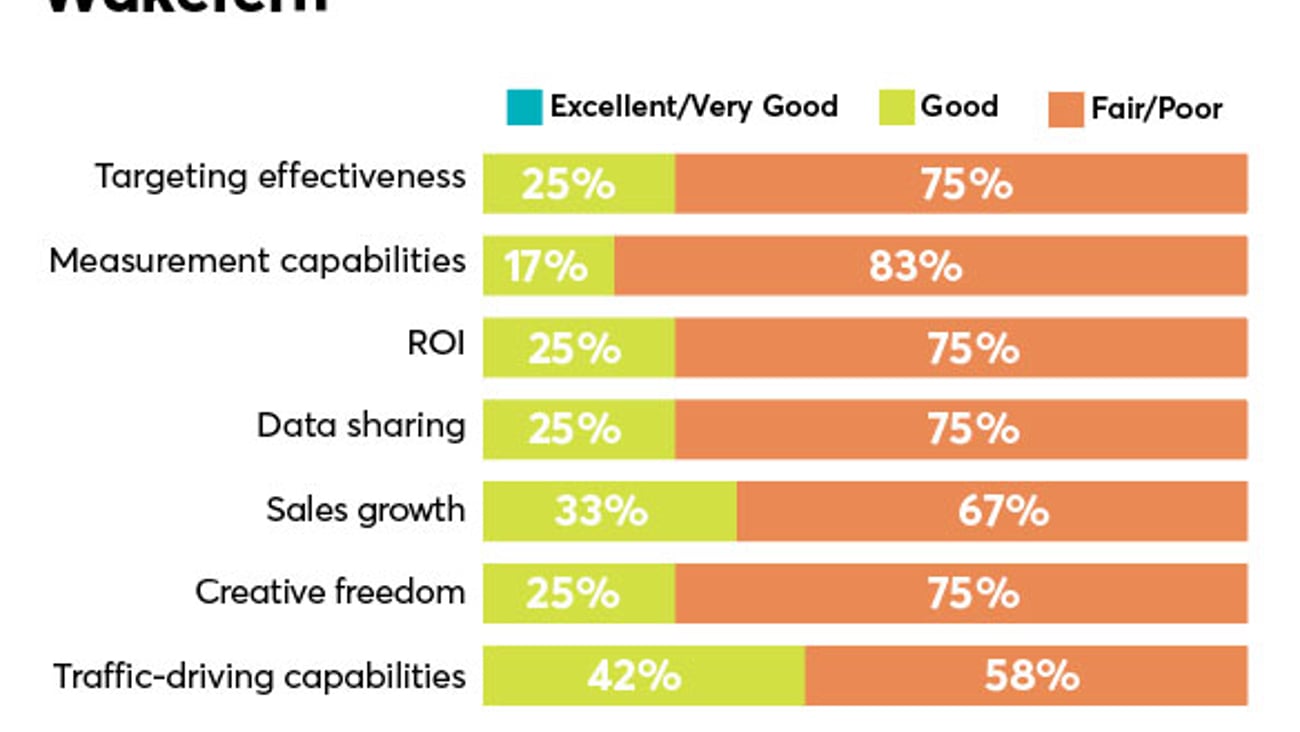

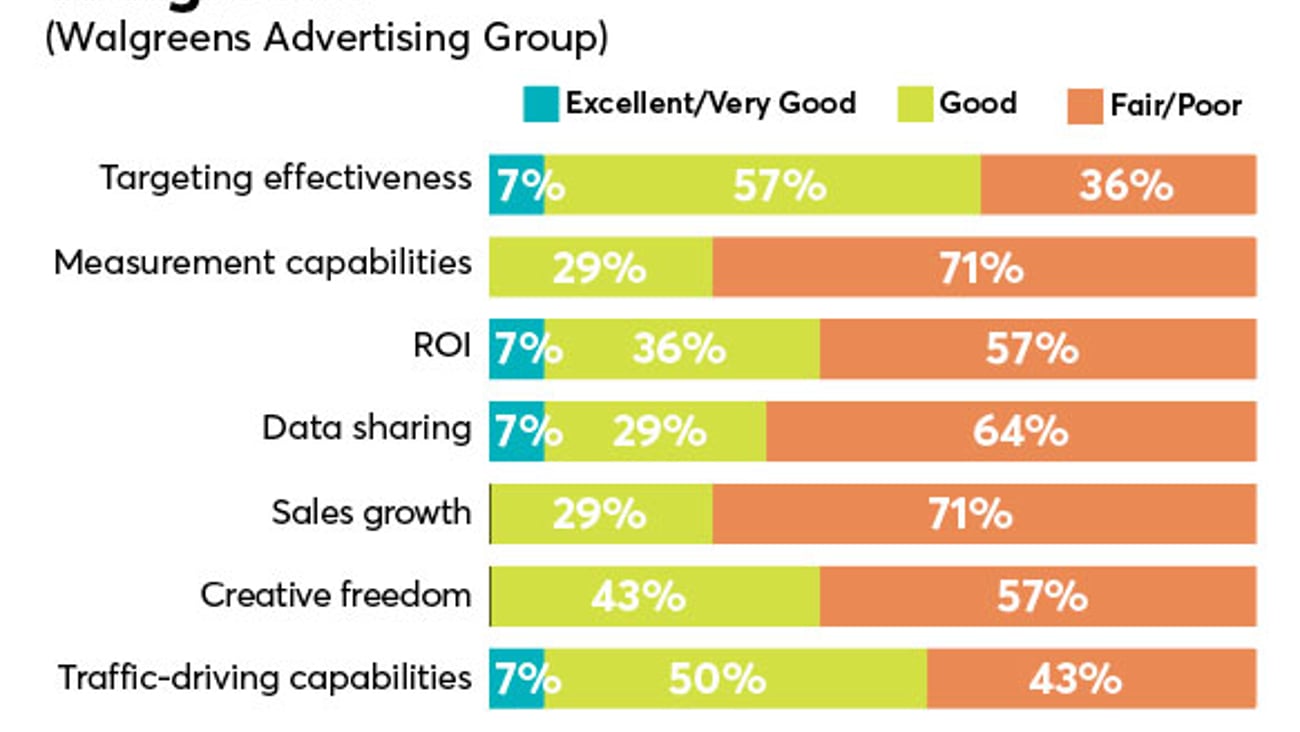

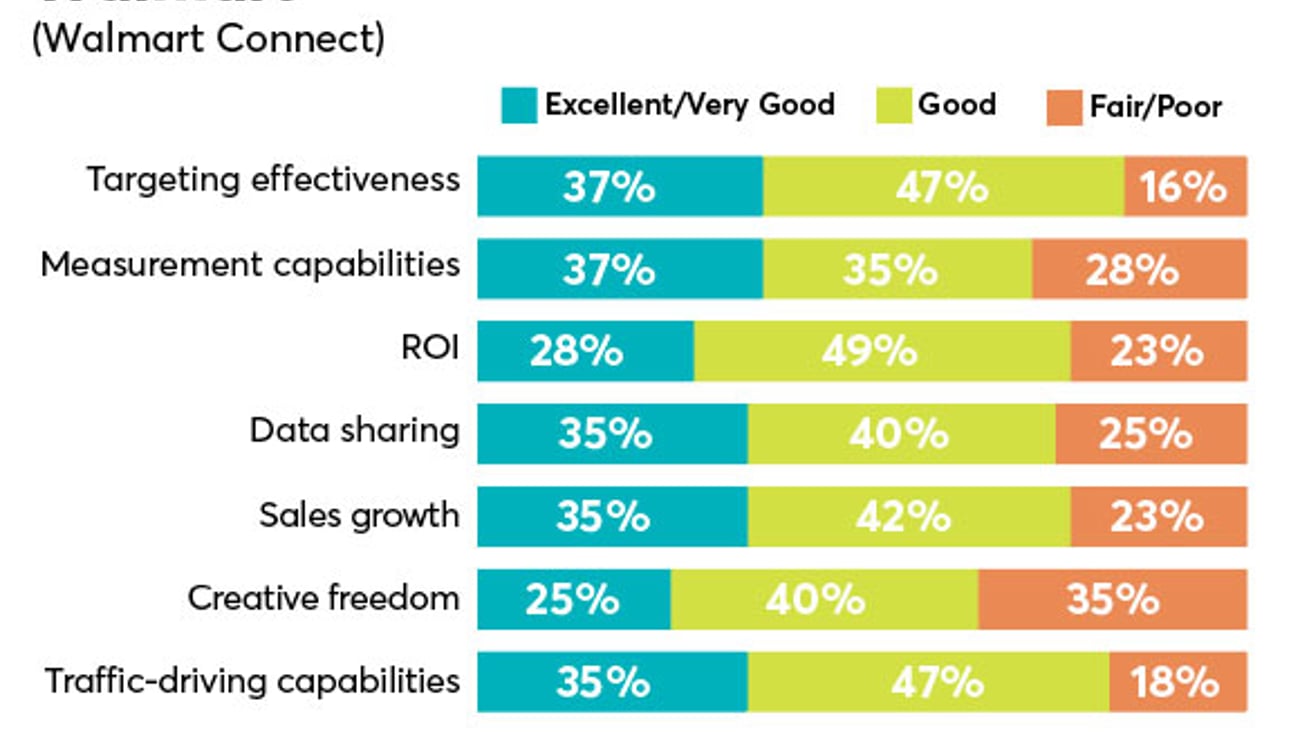

When it came to rating specific RMNs, some stood out above others with regard to specific performance metrics. We asked respondents to rate the retailer media networks with which they work based on their relative strengths in targeting effectiveness, measurement capabilities, ROI, data sharing, sales growth, creative freedom and traffic-driving capabilities.

Not surprisingly, Walmart Connect, Amazon DSP, Target’s Roundel and Kroger Precision Marketing (KPM) were the networks our brand respondents worked with the most followed by Albertsons Media Collective, Instacart Ads and Sam’s Club Member Access Platform.

Among these networks — and all other networks included in the survey — KPM, Amazon DSP and Walmart Connect led the way across all metrics. Comparing these three networks:

• Amazon led the way in targeting effectiveness with 92% of survey participants giving the network at least a good rating in this metric.

• KPM’s measurement capabilities, ROI, data sharing and sales growth performed the best, with at least 80% of participants giving it at least a good rating for these metrics.

• Walmart Connect had a slight edge when it came to traffic-driving capabilities, with 82% of survey takers giving the network at least a good rating for this metric.

Among other noteworthy results:

• More than half of respondents gave Instacart and Sam’s Club at least a good score across all metrics.

• More than half of survey takers gave Roundel at least a good score when it came to traffic-driving capabilities, sales growth, measurement capabilities and targeting effectiveness.

• Meijer generally performed well across most metrics with 62% of survey takers giving the network at least a good score for ROI and creative freedom.

Retail Media Challenges and the Next Frontier

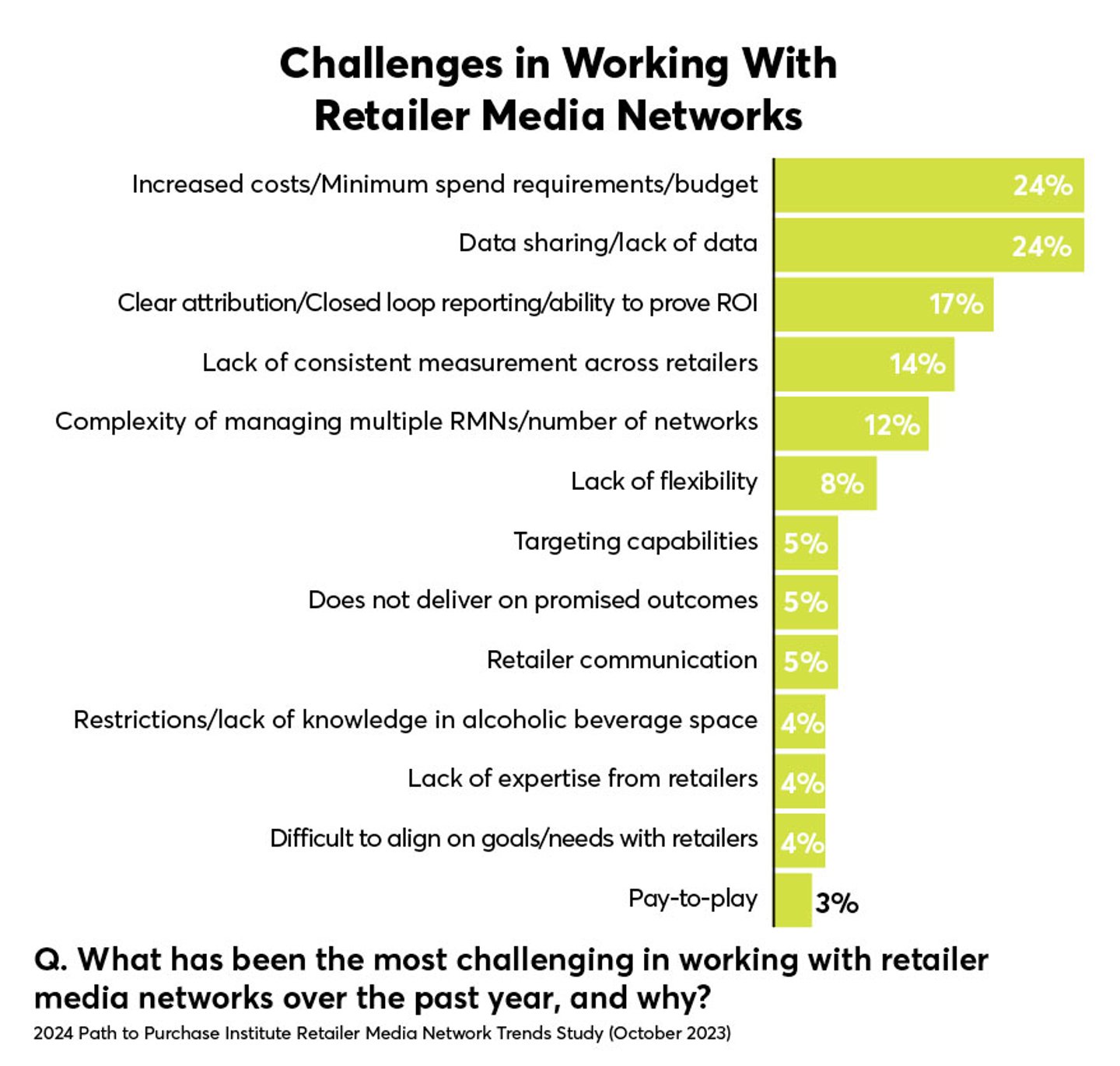

When asked to consider the challenges of working with RMNs, a quarter of survey takers pointed to increased costs, minimum spend requirements and budget, as well as lack of data and data sharing. Also identified by respondents was clear attribution/closed loop reporting/ability to prove ROI and a lack of consistent measurement across retailers.

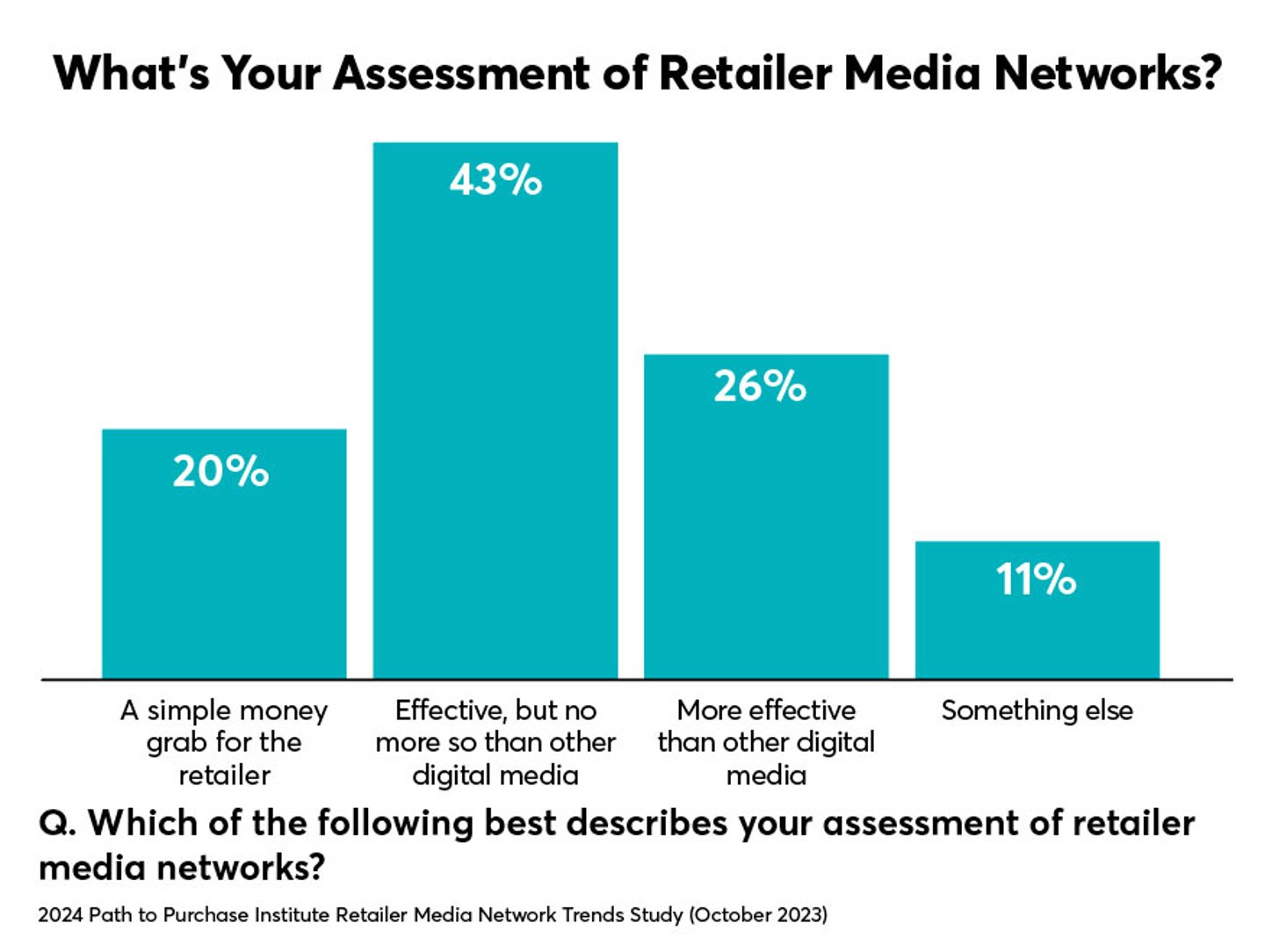

Despite their challenges, 69% of respondents said that RMNs are as effective, or more effective, than other digital media. Breaking it down:

• 43% noted RMNs are effective, but no more so than other digital media. (“We get better exposure and return from social media,” said one respondent.)

• 26% said RMNs are more effective than other digital media. (“There’s a direct tie to sales and more input over how we can pull the strings on specific products to reach certain audiences,” explained a survey taker.)

Skeptics remain, however, with 20% noting RMNs are a simple money grab for the retailer. Program rates and an inability to prove out the ROI of retail media tactics lead some to say retail media is a money grab by retailers. “Customers are demanding buy-in with large investments, but we can’t attribute it to sales,” said one survey taker.

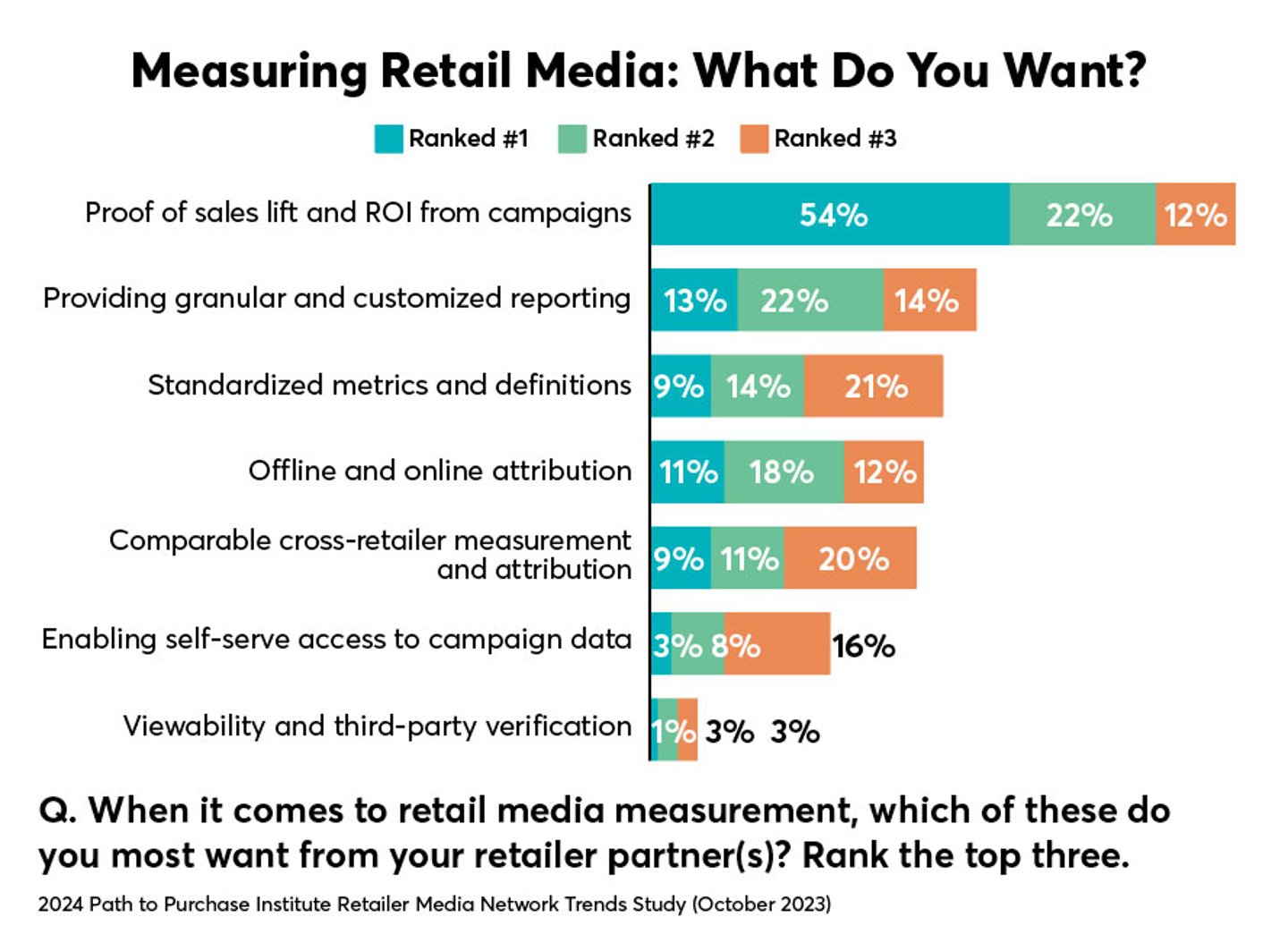

When it comes to retail media measurement, nearly 9-in-10 respondents said they wanted their retailer partner to provide proof of sales lift and ROI for campaigns. Nearly half also indicated they want their retailer partner to provide granular and customized reporting and more than 40% said they wanted standardized metrics and definitions, and offline and online attribution.

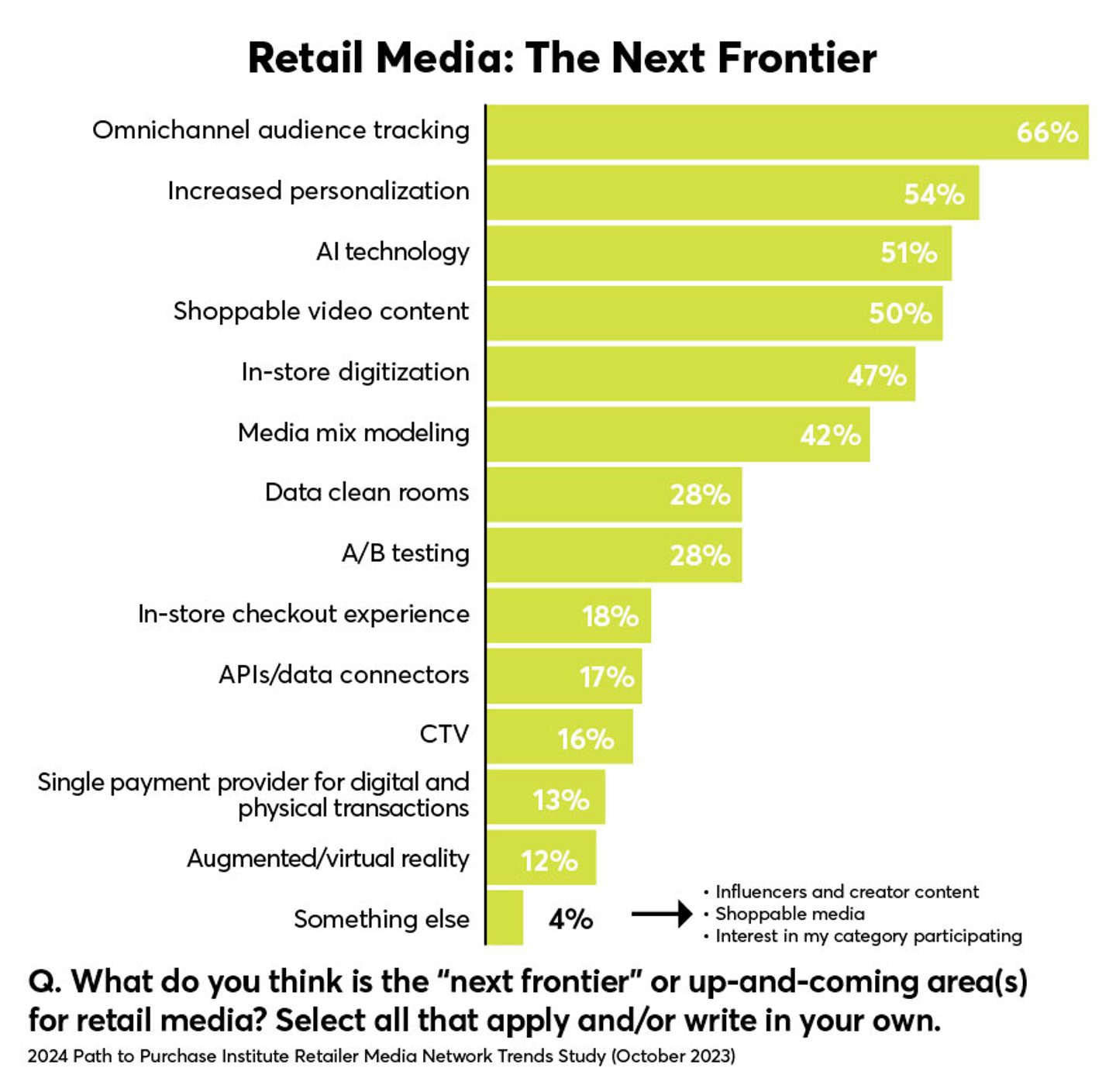

Considering the “next frontier” for retail media, survey takers pointed to an array of tactics and areas. Most notably, 66% highlighted omnichannel audience tracking, followed by increased personalization (54%), AI technology (51%) and shoppable video content (50%).

Check back with the Path to Purchase Institute as we revisit RMNs, shoppable video, AI and other commerce-related hot topics in the second part of our Trends survey in the March/April edition of the magazine.

Organizational Mapping and the Retail Media Opportunity

As the omnichannel landscape continues to grow more complex, we asked survey takers to consider organizational mapping and the retail media opportunity, and how their organization sets up internally. We found CPG organizations are set up to manage retail media in a variety of ways. Some respondents said retail media sits within the shopper marketing team, while others said it is split across sales, e-commerce and marketing. The biggest organizational mapping opportunities identified by respondents focused on increasing collaboration across teams to reduce silos and inefficiencies.

Here’s what some of the respondents had to say on that front …

“Shopper marketing owns retail media planning and execution (as they run point on the marketing relationship with the retailer). Our media team (along with the retail media agency we work with) supports high-level strategy and planning. We like the current setup and have no plans to adjust in the near future.”

“Our organizational set up is extremely poor with low competency of team members, no accountability for performance and little to no integration with other related departments.”

“Retail media falls under the responsibility of marketing and e-commerce. This is an ideal setup as it allows for true omnichannel perspective where the person is not tied to specific accounts, but drives the overall goals and revenue of the brand and business.”

“We are still relatively siloed between marketing and sales, which creates challenges with increased retail media funding, especially when it comes to upper-funnel retail media (i.e., CTV).”

“We don’t currently have a shopper marketing team so retail media gets split between the functioning trade team and above-the-line media — which is ineffective and we’re working on organizational shifts to optimize.”

“Needs improvement. Way too siloed. I’d love to be able to manage the entire retail media budget, instead of having to spend by retailer budget restraints.”